When going through a divorce you must decide what to do with the marital home which represents one of the most crucial choices you face. Yes, you can sell the house. You have three main choices for the property disposition: sell and divide the proceeds or one spouse can purchase the other’s share or maintain joint ownership for a specified time. The financial and legal effects of each choice depend on your individual situation and the legal rules of your state.

The house represents more than financial value because it holds sentimental memories which create additional challenges. The best way to tackle this is to break it down. Let’s walk through the options to help you find the clearest path forward.

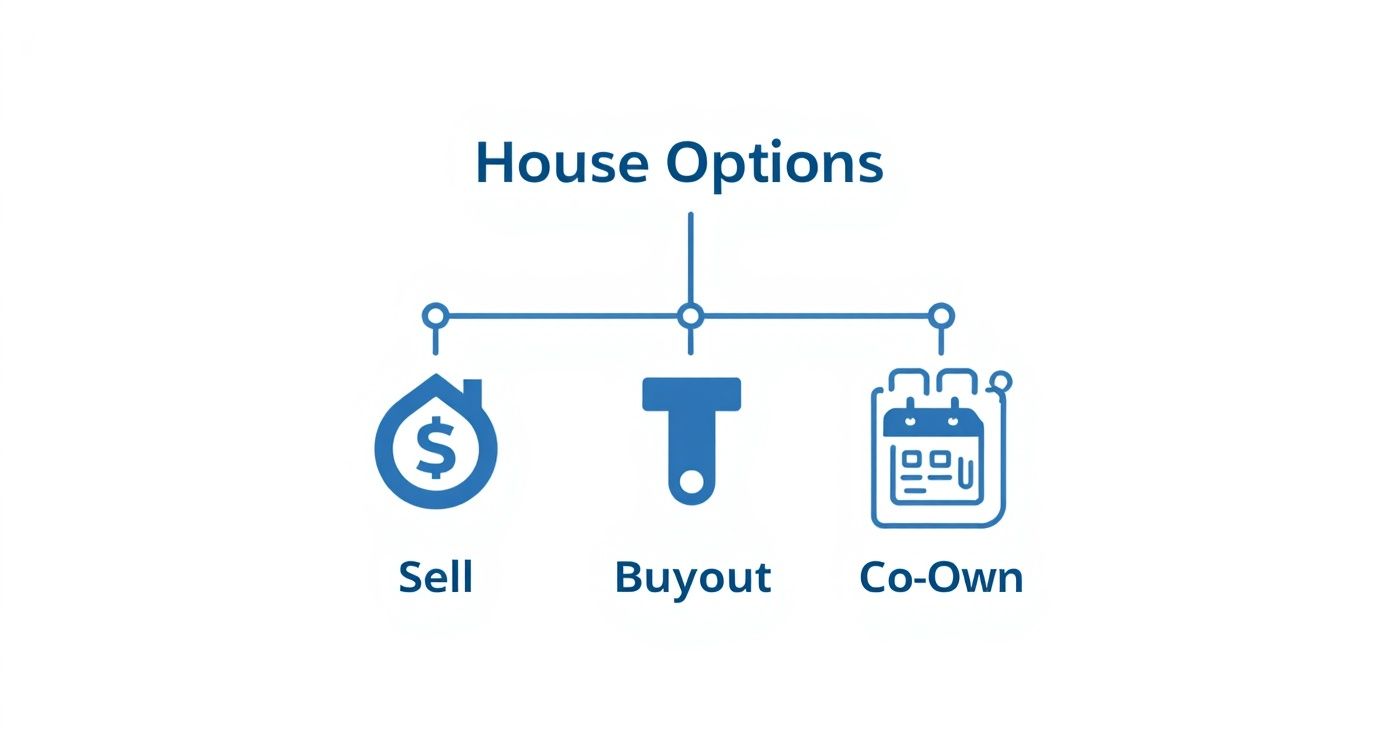

Your First Step: Deciding What to Do with the House

The financial impact of handling the marital home creates a major burden during what should be an emotionally challenging period. Your key objective involves moving past your overwhelming feelings to create simple choices that you can handle. Gaining control starts with objectively looking at your options.

The first decision you must make tends to be the most difficult one to make. Your goal is to break down all financial connections and emotional bonds and shared plans for the future in one process. For more on the legal side of this process, this comprehensive guide to selling your home during a divorce is a really solid resource.

Here’s a simple breakdown of the three main routes you can take:

The house sale leads to a complete financial separation according to the data. But for some families, especially those with kids, a buyout or temporary co-ownership might offer much-needed stability.

Comparing Your Options

Let’s dig into what each of these choices actually looks like in the real world. The right decision for you and your ex-spouse comes down to your specific situation—your finances, how well you can communicate, and what you both want for the future.

Here is a quick look at how the three paths compare.

Comparing Your Home Sale Options During Divorce

| Option | Best For | Key Challenge | Typical Timeline |

|---|---|---|---|

| Sell & Split | Couples who need both financial separation and cash to begin their new life. | Agreeing on a listing price, an agent, and accepting an offer. | 2–6 months |

| Buyout | One spouse who is financially stable and wants to keep the home (often for children). | The buying spouse needs to either qualify for refinancing or have enough cash to pay out the equity. | 1–3 months |

| Co-Own | Parents who want to maintain stability for their children for a set period. | Creating a rock-solid legal agreement and managing shared expenses without conflict. | 1–18+ years |

The table demonstrates that no universal solution exists because each person needs to find the answer that fits their particular situation.

Now, let’s explore these in a bit more detail.

-

The simplest way to divide assets after divorce is to sell the house and divide the proceeds between the parties. You sell your most valuable shared property to pay off the mortgage and all joint debts before taking your share of the money to start your new life. The agreement creates a complete financial division between the two parties.

-

One Spouse Buys Out the Other: This option is great for providing stability, as one person (and the kids, if you have them) gets to stay in the home. The big hurdle here is financial. The spouse who wants to keep the house has to be able to qualify for a new mortgage on their own or have enough separate funds to buy out their ex-partner’s share of the equity. In some cases, a loan assumption can be an alternative to a full refinance, so that’s worth looking into.

-

The house remains under joint ownership between the parties. People often describe this as a “deferred sale.” This is a typical arrangement where parents agree to keep their children living at home until they reach a certain age or complete their education. The arrangement needs a complete legal contract which defines all aspects of mortgage payments and tax responsibilities and insurance and maintenance costs and the exact timing of house sale.

The most important piece of advice I can give is to not let emotion drive the bus. Animosity will absolutely tank the final sale price. Treating the sale as a business deal will lead to the highest possible sale price and the easiest closing process.

The Legal and Financial Truths You Need to Know

Before you even think about putting a “For Sale” sign in the yard, you have to get a handle on the legal and financial rules of the game. Selling a house during a divorce isn’t just a real estate transaction; it’s a legal process. The rules determine who receives what and learning them stands as the only way to make sure everything gets handled fairly.

The process seems complicated but it actually depends on several main principles. The law does not recognize a “family home” because it treats all marital property as assets which must be divided according to the laws of your state.

This part of the process often sparks major conflict, especially when you’re also trying to figure out new living arrangements. Our article on who has to leave the house in a divorce provides detailed information for this particular situation.

Marital Property vs. Separate Property

The first, most critical distinction you need to make is between marital property and separate property. The single concept of separate property determines which assets will be included in the division process.

-

Marital Property: This is pretty much everything—assets and debts—that you or your spouse acquired during the marriage. The source of funding and ownership details do not matter in this situation. The property you acquired during your marriage will most likely be considered marital property unless you can prove otherwise.

-

Separate Property: This is stuff that belonged to one spouse before the marriage. The definition of separate property also includes any inheritance or gifts that were given to one spouse during the marriage.

But even this can get messy. The house was separate property of your spouse before marriage but you both used joint funds to pay mortgage and renovate kitchen for ten years. The home’s value has transformed into marital property through the legal process of transmutation.

Here’s a real-life scenario: Sarah owned a condominium before she met and married Tom. They lived there together for a decade, using money from their joint checking account for the mortgage and a big kitchen remodel. Even though the condo was originally Sarah’s separate property, the value they added together is now likely marital property, and Tom has a legitimate claim to a piece of it.

Community Property vs. Equitable Distribution: What’s Your State’s Rule?

Your property division will follow the legal rules which apply in your state. Every state follows one of two systems, and the difference is huge.

-

Community Property States: Only a handful of states (like California, Texas, and Arizona) follow this rule. The law treats all marital property as equally owned between spouses. The assets you own together with your spouse will be divided equally when you divorce.

-

Equitable Distribution States: Most states use this model. The courts in these states allow judges to distribute property based on their understanding of what constitutes a fair and equitable distribution. The key thing to remember is that “fair” does not automatically mean a 50/50 split.

So, what does a judge consider “fair”? Your agent will evaluate the entire situation by examining these factors: Your marriage duration. Your current health status together with your spouse’s health status. Your present income along with your anticipated future earnings. Your non-financial contributions such as your role as a stay-at-home parent. Your spouse’s misuse of marital funds represents bad conduct.

The final distribution of home sale proceeds in an equitable distribution state may result in different percentages such as 60/40 when a judge determines the situation requires it.

The Divorce Appraisal: Your Non-Negotiable Starting Point

The accurate unbiased home value serves as the critical information which enables you to make progress regardless of your location. The specialized appraisal service functions as the essential requirement which enables these outcomes to happen. A professional divorce appraisal needs to be done because it helps determine the actual value of your property. The formal appraisal process conducted by certified appraisers produces legally binding property valuations which differ from the brief market analysis done by real estate agents.

The evaluation creates the financial base which serves as the foundation for all subsequent negotiations. The appraised value creates the basis for buyout calculations and equity distribution and final asset division which relies on data instead of emotional assumptions. The global divorce appraisal service market experienced a sudden surge in demand because it reached a value of $1.5 billion in 2023 and analysts predict it will almost double by 2032.

Agreeing to hire a neutral, certified appraiser from the very beginning can save you an incredible amount of time, money, and conflict. The argument about the house’s worth becomes irrelevant when you have a neutral certified appraiser handling the case.

How to Manage a Traditional Home Sale Together

https://www.youtube.com/embed/zlg8j2mOQ70

Deciding to sell your home on the open market means you’ve agreed to work toward a common financial goal, even when everything else feels uncertain. The journey to success proves difficult yet it becomes possible when you maintain the proper mental attitude. Your success in this sale will depend on treating it as a business deal instead of an extension of your divorce.

Think of it as a joint business venture. The goal is simple: get the best price for your shared asset in a reasonable amount of time. The key to success in this venture depends on separating emotional elements from the operational aspects of selling a house.

The family home stands as the most valuable asset for the majority of couples. The sale of your home will determine your financial future because it constitutes 60-70% of your total net worth. The shared goal between you and your partner will keep you both focused on your current tasks.

Finding the Right Real Estate Agent

Your first—and most important—decision is finding a neutral real estate agent. The individual performs duties that go beyond sales duties because they manage projects and lead you through the complicated process. The current situation does not support hiring someone from your personal connections. You need a seasoned professional who has specific experience with divorce sales.

An agent who has dealt with these situations before will understand the communication challenges and legal requirements that arise in these cases. The agents use their knowledge to keep both parties informed while resolving pricing and offer disagreements and working with each other’s legal representatives.

When you’re interviewing agents, be direct. Ask them things like: How many divorce sales have you handled in the last year? What’s your process for communicating with two sellers who live separately? How do you manage disagreements between spouses over an offer or inspection repairs? Can we speak with a few of your past clients who were in a similar situation? Their answers will tell you everything you need to know about their experience and their ability to stay neutral. A great agent acts as a buffer, keeping the deal professional and moving forward.

Setting the Price and Preparing the Home

The first major obstacle emerges when you attempt to establish an asking price. One spouse wants to set a high price for the best possible return but the other wants to sell fast to end the process. This is where you have to lean on your agent and the data.

Your decision should be based on a comparative market analysis (CMA) your agent prepares. This report isn’t based on emotion or opinion; it shows exactly what similar homes in your neighborhood have sold for recently. The data serves as the most effective way to find common ground.

Once you have a price, you need a plan to get the house ready. Work together to decide which repairs or cosmetic updates are truly necessary to attract buyers. Create a clear budget and a timeline so no one feels stuck with all the work or financial burden.

Pro Tip: Open a temporary joint bank account just for home-sale expenses. Both of you can deposit an agreed-upon amount to cover things like repairs, staging, or deep cleaning. It keeps everything transparent and stops money arguments before they start.

Navigating Showings and Offers

Coordinating showings can be a headache, especially if one of you is still living in the house. The best approach is to agree on a fixed schedule for when the house can be shown and stick to it. A shared digital calendar is a simple tool that can prevent a lot of conflict and confusion.

When an offer comes in, your agent should present it to both of you at the same time, whether that’s on a conference call or in a joint meeting. The discussion should proceed in a professional manner while focusing on the numerical aspects of the deal including price and contingencies and closing date. The success of your house sale during divorce depends on making communication work between you and your spouse; several resources exist to help you develop better communication during times of conflict.

Co-Selling Success Checklist

A simple checklist can be a lifesaver, giving you both a neutral guide to keep things focused and organized.

- Agent Selection: Have you both interviewed and agreed on a neutral agent with divorce sale experience?

- Communication Plan: Is there a clear plan for how and when you’ll get updates from the agent (e.g., a weekly summary email)?

- Financial Plan: Do you have a joint account for expenses with agreed-upon contributions?

- Preparation Plan: Have you agreed on a list of necessary repairs and a firm budget?

- Showing Schedule: Is there a set schedule for showings that both parties have approved?

- Offer Review Process: Have you agreed to review all offers together with your agent present?

Throughout this process, remember that agent commissions will be your biggest closing cost. Knowing how these fees work is crucial. The complete breakdown of real estate commissions and their effect on your sale proceeds appears in our guide. The traditional sales process demands a significant amount of work but it becomes possible to complete it with a well-structured plan and expert guidance.

Exploring Faster Sale Options for a Clean Break

The traditional home sale process seems to be a difficult process when you look at it honestly. The endless showings, the nit-picky negotiations, the constant need to keep the house perfect—it’s a lot for anyone. The daily routine of divorce makes life seem impossible to handle. The relationship stays stuck in the past which extends emotional pain and creates new battles that prevent you from moving forward.

The good news? The open market isn’t your only path forward. There are faster, much more direct ways to sell your home during a divorce. The options focus on speed and certainty and simplicity to provide a quick solution instead of extracting maximum value from the sale. These documents exist to help you and your ex-spouse finish your divorce case quickly so you can begin your new lives.

How Selling to a Cash Home Buyer Works

One of the most popular alternatives is selling directly to a cash home buyer. The real estate investor or company that purchases properties using their own capital represents this category. Because they aren’t relying on a bank loan, the entire transaction is fundamentally different. Their mission stands to eliminate the numerous stages which buyers encounter during their shopping journey.

Here’s what makes this route so appealing during a difficult time:

- No Showings: You get to skip the parade of strangers through your home. The method lets you handle your existing responsibilities while reducing your overall stress levels.

- No Repairs: Cash buyers purchase homes “as-is.” You won’t have to argue over inspection reports or come up with money for repairs you can’t afford.

- Guaranteed Closing Date: This is a big one. Since there’s no lender involved, you don’t have to worry about financing falling through at the eleventh hour. You get a firm closing date, often in just a couple of weeks.

This approach gives you a level of predictability that’s invaluable when you’re trying to finalize a divorce settlement and figure out what’s next.

The Trade-Off: Speed vs. Price

The convenience of online shopping comes with a cost. The main trade-off when selling to a cash buyer is that the offer will almost certainly be below what you might get on the traditional market. This isn’t a bait-and-switch; it’s just part of their business model.

Cash buyers have to bear all the risks that come with the transaction. They will handle all repair costs and holding expenses and perform the required work to sell the property at a later date. The offer needs to include all these elements to give you an immediate guaranteed payment which comes at the cost of a reduced sale price.

The choice comes down to a strategic decision. Your situation will determine which option emerges as more important: getting the highest possible price or reaching a quick agreement that enables both of you to start fresh.

The financial benefits of avoiding joint ownership disputes surpass the value of the price difference for many divorcing couples. The process enables you to achieve an immediate and final resolution of your most valuable shared asset. Our comprehensive guide explains when cash sales become the optimal choice for selling a house.

When a Cash Sale Makes Sense in a Divorce

The cash sale method works best for certain divorce cases which commonly occur during separation proceedings.

The following situations require you to think about direct sales:

- High-Conflict Situations: If communication has completely broken down, a direct sale means you don’t have to agree on showings, offers, or negotiations.

- A Need for a Quick Financial Split: When one or both of you need the equity from the home to find a new place to live or pay off debts, a cash sale delivers those funds in weeks, not months.

- A Home in Disrepair: If the house needs a lot of work and neither of you has the money or emotional energy to manage renovations, selling “as-is” is the most practical way to wash your hands of the problem.

The certainty and speed of a cash sale prove to be extremely beneficial in these situations. Eagle Quick For Cash is a company that operates specifically in this area. The process is incredibly simple: you request a no-obligation cash offer, and if you accept it, you can close on a timeline that works for you. The method provides a valuable option for those who want to end their shared property investment with complete efficiency.

How Market Conditions Can Impact Your Sale

A house sale during divorce proceedings operates under special conditions which separate it from standard real estate transactions. Your decision will be based on your personal preferences but financial results will depend on the current state of the real estate market. Your sale success will depend on three crucial market elements which include interest rates together with the number of available homes in your area and buyer confidence levels.

Understanding these outside forces is critical. The current market conditions show that sellers have the upper hand because buyers tend to compete for available homes. The market operates in two main ways: a seller’s market where homes receive multiple offers and a buyer’s market where properties remain unsold for extended periods. The answer will shape your timeline, pricing strategy, and even the best way to sell the property.

Seller’s Markets vs. Buyer’s Markets

The traditional sales process follows distinct procedures which depend on market conditions. The environment creates unique opportunities and challenges for divorcing couples.

-

The market conditions create a seller’s market because there are more buyers than available homes which leads to quick sales at high prices. The process of evaluating multiple offers under time pressure will lead to new disagreements between you and your partner.

-

In a Buyer’s Market: When there are more homes for sale than active buyers, your property might linger. The extended process of divorce settlement negotiations forces you to maintain financial and emotional ties to your ex for longer periods which creates additional stress about handling mortgage payments and property maintenance and negotiating price reductions.

Major economic changes create actual consequences. Research has shown that U.S. divorce rates dropped temporarily during the Great Recession. The financial problems made it impossible for couples to separate and divide their home property.

The process of buying and selling property requires a delicate balance between market timing and personal circumstances.

Real estate professionals commonly suggest waiting for market timing to achieve the highest possible sale price. The luxury of waiting for the perfect market conditions to sell your house becomes unavailable when you go through a divorce. Your personal timeline—the urgent need for financial closure and emotional separation—usually has to come first.

The search for ideal market conditions might lead you to stay financially tied to your ex for an extended period that exceeds what is necessary. The delay prevents both of you from achieving genuine progress in your lives.

The actual inquiry extends beyond choosing the right timing for selling because it involves determining the complete expenses of enduring the situation. The time and emotional stress of selling at a loss can lead to expenses that go beyond what you could gain from selling at market prices.

You must evaluate your choices in this situation. A traditional sale might bring in top dollar in a hot market, but it’s loaded with uncertainty and takes time. The slow market conditions together with your aversion to lengthy sales should lead you to select a faster selling option. Our guide on how to sell your house quickly provides practical solutions for those who want to sell their home fast.

The present market conditions make selling to Eagle Cash Buyers the best option for couples who are buying or selling during a buyer’s market and for those who are going through a contested divorce. A cash offer is based on the home’s current “as-is” condition, giving you a guaranteed price and a firm closing date, no matter what interest rates or the local market are doing. The path delivers certainty and speed to those who require these elements most.

Answering the Tough Questions About a Divorce Sale

Even with the best intentions, selling a home during a divorce is a minefield of “what-ifs.” The home sale takes place under uncommon conditions which include legal barriers and financial dangers. The process of finding direct answers to typical questions helps you create a plan which prevents major conflicts from developing.

The following problems represent the most typical relationship challenges that couples face according to my analysis. These aren’t just hypotheticals; they’re real-world problems with established legal solutions.

What Happens If My Spouse Refuses to Sell the House?

The following situation represents the most serious case that leads to sleepless nights for numerous people. But let me be clear: you are not stuck. If you’re ready to sell and your spouse digs in their heels, the legal system has a direct remedy.

Your attorney has the ability to file a motion which would force the sale to proceed. A family court judge possesses the authority to order the house sale even if one party refuses to agree. The court’s main objective is to achieve an equitable distribution of property which means it will not allow a deadlock to persist.

The court can designate a neutral third party known as a receiver or special master to take control in highly contentious situations. The person has the authority to sign listing agreements and handle offer negotiations and final sale transactions without needing approval from the uncooperative spouse.

Who Pays the Mortgage While the House Is for Sale?

The immediate and crucial problem exists at this point. Your missed payments will damage your credit scores and endanger your home which serves as your main financial asset. You need to decide—either by agreement or through a court order—who will cover the mortgage, taxes, and insurance while the home is on the market.

There are a few common ways to handle this:

- Keep Splitting: You both continue to contribute to the payments just as you did during the marriage.

- One Spouse Pays: The person still living in the house often covers the costs, usually with an agreement that they’ll be reimbursed from the sale proceeds.

- Use a Joint Account: You can fund a separate joint account specifically for these housing expenses to keep everything transparent and straightforward.

If you can’t agree, don’t let it slide. Your lawyers will need to ask the court for a temporary order that spells out exactly who is responsible for what. Get this in writing, no matter what.

How Are the Profits from the Sale Divided?

The final sale price will not divide evenly between the two parties. Dividing the proceeds is a methodical process, and the final numbers are determined by your divorce decree.

First, all the property’s debts get paid right off the top. The outstanding mortgage balance together with any home equity lines of credit (HELOCs) and other liens and the standard seller closing costs and transfer taxes need to be included.

What’s left over is the net proceeds—the actual cash to be divided. The money distribution between you and your spouse will follow the laws of your state which either follow community property rules or equitable distribution principles and your settlement agreement. The division will be modified to compensate one spouse who used their separate pre-marital funds for the down payment.

Can We Sell the House Before the Divorce Is Final?

Yes, absolutely. In fact, it can be a brilliant strategic move. The process of selling your house before divorce finalization turns your most valuable asset into cash. The system eliminates all uncertainty from the process which enables you to handle final negotiations with complete clarity about your available funds.

Both parties need to maintain complete agreement about the terms of this arrangement. The parties must reach consensus on three major aspects which include the listing price and the choice of real estate agent and the method for handling offers.

The funds from the sale will not be deposited into your individual bank accounts. The money is typically kept in an escrow account which is managed by a third party. The funds will remain frozen until a judge signs the final divorce decree which will establish the exact distribution of the money.

The process of dealing with these questions demonstrates the value of a simple low-conflict sale. A direct path to your goals will help you survive when both your life logistics and your emotional state become too much to handle.

The process of home selling can become overwhelming for those who face repairs and showings and lengthy negotiations. A cash sale enables you to avoid the entire standard sales process. The method provides certainty to both parties which helps them finalize their divorce and move on with their lives. Eagle Quick For Cash offers a no-obligation cash offer for your home which you can accept to secure a guaranteed closing date. Learn more about how we can help at https://www.eaglecashbuyers.com.