When life throws you a curveball—like a job loss, an unexpected illness, or another financial crisis—keeping up with your mortgage can suddenly feel impossible. The initial stage of solving your problem requires you to identify all available options which exist for your current situation.

One of the most common solutions is a loan modification. The process involves an established method which allows you to modify your original mortgage agreement into a new permanent agreement that your lender will accept to lower your monthly payments. The program exists to help you keep your home while it works to stop the foreclosure process.

What Is Loan Modification In Simple Terms

Your mortgage exists as a contract which you entered into under different conditions than what you face now. The original agreement between us became impossible to maintain when life took a new direction. A loan modification exists as an official document which enables you to modify the original agreement that you signed.

This agreement does not create a new loan for you and it does not allow you to refinance your existing loan. Your current mortgage stays in place while your lender agrees to modify the loan terms which match your changed financial situation. Homeowners who face financial difficulties use this established method to protect their properties although it does not demonstrate that they have failed.

How Does a Loan Modification Work

The main objective requires you to reduce your mortgage payments which you must pay each month. Your lender has multiple tools at their disposal to reach this goal and they tend to combine these tools for creating an effective solution which suits your needs.

Lenders have three main factors which they use to lower your payment amount.

How a Loan Modification Can Change Your Mortgage

| Modification Type | How It Reduces Your Payment |

|---|---|

| Interest Rate Reduction | The program reduces your interest rate which decreases your total monthly payments. |

| Loan Term Extension | The loan term extension option allows you to spread your remaining loan payments over an extended duration which can extend from 20 years to 30 or 40 years thus reducing your monthly payment amount. |

| Principal Forbearance | A portion of your principal is set aside. You won’t pay interest on it, and the lump sum is due when you sell, refinance, or pay off the loan. |

The loan modification process leads to a legally binding contract which replaces your current mortgage agreement. The legal process behind these changes becomes clear when people learn the basic principles of addendum writing because they understand how to create formal contract modifications.

A loan modification is not a new loan. The process changes your current debt structure to develop a payment schedule which helps you protect your home while you achieve financial stability.

The tool offers powerful features which make it an excellent resource but users can select from various other alternatives. You should compare it with other options including cash home sales because these methods might deliver faster solutions with higher certainty depending on your specific circumstances.

Why Loan Modifications Became A Lifeline For Homeowners

The loan modification process needs you to understand its original beginning which explains its current structure. The practice used to be uncommon. Homeowners who faced financial difficulties before the mid-2000s had limited options because foreclosure became their most common and fastest path to losing their homes.

Two key events transformed the entire situation during the 2008 global financial crisis. The housing market collapse forced millions of Americans to face the threat of losing their homes. The widespread foreclosures forced lenders and homeowners and government officials to realize that these home losses were creating two major problems which threatened to destroy both local communities and the entire economy.

A New Approach To Foreclosure Prevention

The crisis brought forth a fresh perspective which people began to adopt. Instead of seeing foreclosure as the only answer for a missed payment, lenders and policymakers realized there was a much smarter path: working with homeowners. The process resulted in official loan modification programs which banks established to create solutions that would benefit all parties involved.

The idea behind it is pretty straightforward. The foreclosure process creates a disorganized situation which costs everyone involved a lot of money. The financial losses which lenders face together with home losses experienced by families and vacant properties in neighborhoods create a chain reaction of negative effects. A successful loan modification process enables families to stay in their homes while it transforms their delinquent loans into performing loans. It’s a true win-win.

Seeking a loan modification is not an admission of personal failure. The program offers a sanctioned financial approach which enables responsible homeowners to handle large economic downturns and sudden personal financial emergencies.

The backstory stands as an essential element. The document proves that the process you want to use stems from a proven system which has already been tested in actual situations. The tool functions as a proven economic instrument which helps homeowners while keeping the housing market stable.

The Impact Of Modern Modification Programs

These programs have become essential to the housing market recovery since their introduction at a large scale. The program delivered vital support to numerous families which stabilized the market while stopping the situation from getting worse. The data presents a clear narrative.

Fannie Mae and Freddie Mac serve as examples. The organization has finished 2,788,002 permanent loan modifications since they started their work in September 2008. The program achieved 7.2 million foreclosure-prevention activities through its complete operational system. The foreclosure prevention programs need further investigation because they show the full extent of the commitment which went into these efforts.

The historical context shows that loan modification process exists beyond its basis as a financial transaction. The solution emerged from a national emergency which completely altered how the housing sector delivers support to individuals who face financial difficulties. The home sale process has two main paths which people use to sell their homes but cash sales offer a faster and more reliable solution based on individual circumstances.

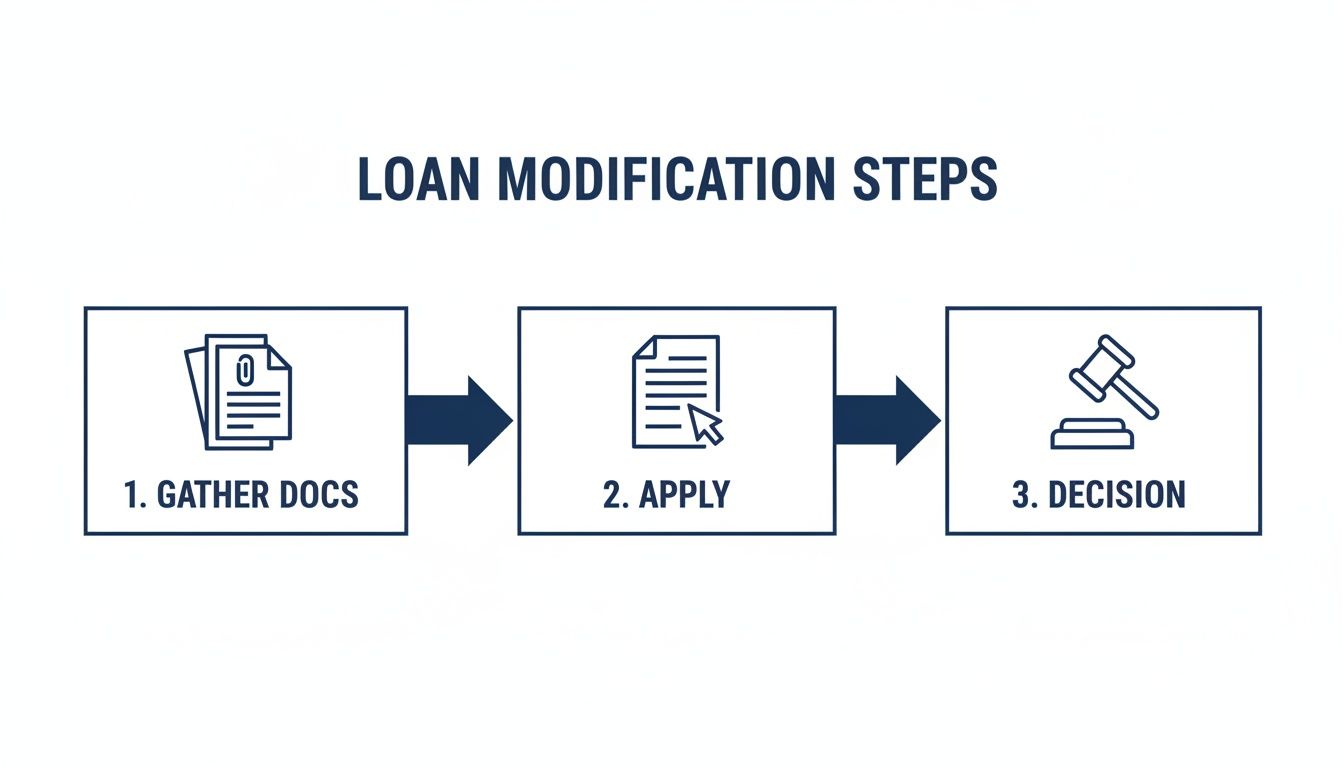

Navigating The Loan Modification Application Process

You can handle the mortgage modification request to your lender by following a simple step-by-step process which breaks down this task into easy-to-understand components. The preparation for a big job interview requires you to do your best because it helps you build confidence which makes you stand out as an excellent candidate.

Your lender requires proof of two essential things through this application process. First, you need to demonstrate that you have encountered genuine financial difficulties and second, you must prove that you possess enough stable income to manage the new affordable payment plan.

Your first move is to call your lender or mortgage servicer (the company you send your payments to). You need to inform them about your financial difficulties because you want to understand all available options including loan modification. The process starts when they send you an application package.

Proving Your Eligibility

You need to understand what your lender wants before you start dealing with all the paperwork. The lender requires you to prove why your current financial situation prevents you from continuing to make your original mortgage payments. The modified payment system needs you to prove that you can make regular payments of the new amount.

Lenders will assess various common difficulties which borrowers face during their assessment process.

- Loss of Income: Getting laid off, having your hours cut, or a seasonal job ending.

- Major Life Events: Things like a divorce, the death of a spouse or co-borrower, or a serious illness or disability that impacts your finances.

- Increased Expenses: A sudden spike in medical bills or other essential costs you couldn’t have planned for.

- Disaster Impact: Your home being damaged in a natural disaster, creating unexpected financial strain.

You must provide evidence which shows your income will stay steady enough to cover the new payment amounts. Lenders don’t need you to have perfect financial status but they want to confirm that your loan modification payments will keep coming for the entire duration of the modification.

Assembling Your Financial Story

Your main task begins when you receive the application packet because you need to collect all required documents. The main work happens at this stage so you must dedicate yourself to thoroughness. Your goal is to give the lender a complete and honest snapshot of your financial life.

Your application contains more than just papers because it explains your financial difficulties together with your strategy to regain financial stability. The documents you submit serve as evidence which demonstrates why a modification would benefit both you and your lender.

The following documents exist as standard requirements which you will need to show:

- Proof of Income: Your most recent pay stubs, W-2s, or if you’re self-employed, profit-and-loss statements.

- Tax Returns: Your last two years of federal tax returns, fully signed and dated.

- Bank Statements: The last two to three months of statements from all your bank accounts to show your cash flow.

- A Detailed Hardship Letter: This is your personal statement. Explain what happened, why you fell behind, and why you’re confident you can make a modified payment. Be direct, clear, and truthful.

- A Household Budget: A simple list of all your monthly income and expenses. This shows the lender exactly where your money goes.

The most critical error which people commit involves submitting incomplete or disorganized applications. The process will take its course until you experience a complete delay or your application receives a denial. Check every page thoroughly to verify that all signatures and dates exist and that all fields have been completed before you submit your document.

Homeowners who need to stop an upcoming auction must learn how to stop a foreclosure auction because filing for a modification does not create an automatic stop to the process.

A modification serves as an excellent solution for many people yet it does not represent the sole available option. You should explore alternative solutions because the process continues for an extended period and you anticipate your financial situation will not improve. Selling your home for cash serves as an alternative which provides an immediate and guaranteed solution that avoids the need for lender authorization and payment schedule extension.

The Pros And Cons You Need To Consider

You need to assess all aspects of a loan modification before making this essential financial choice. The payment support function serves as a financial lifeline which helps people who face difficulties in making their payments. The program presents two separate systems which each come with their own set of advantages and disadvantages which will affect your life for an extended period. The analysis will show you the positive aspects and negative aspects which will help you choose the right option for your particular situation.

The journey itself has a few key milestones. The basic path you need to follow appears in this quick flowchart.

The process of obtaining a decision from your lender after you begin document collection requires both time and extensive organizational work.

The Advantages Of A Loan Modification

The main benefit of a successful loan modification allows you to maintain ownership of your home. The process works as a full stop to foreclosure which enables you to regain your essential feeling of security.

The modification process brings immediate relief to you while it allows you to save your home.

- The payment system becomes affordable to you through this process which represents the program’s main objective. The program enables you to decrease your mortgage payments until they become affordable for your financial situation.

- The program enables lenders to reduce their interest rates which results in customers saving thousands of dollars throughout their loan term.

- The program allows you to avoid foreclosure which protects you from the severe emotional and financial costs of losing your home.

- A loan modification creates less credit damage than foreclosure because it enables you to handle your debt but it will still negatively affect your credit score.

The Disadvantages And Risks To Know

The system presents numerous benefits yet users need to understand all possible negative aspects which exist. The loan modification process involves an extensive process which lacks any magical powers.

The application process stands as the initial step which will take you through a long and frustrating journey. You could be waiting months for an answer, with absolutely no guarantee of approval at the end. The process requires you to handle a large amount of paperwork and missing one essential document will force you to start the entire application process again.

Financial decisions require you to evaluate all available options.

- Your credit score will decrease because of a loan modification. Lenders report it to the credit bureaus as a restructured debt, which tells other potential creditors you had trouble paying as originally agreed.

- To get those payments down, lenders often stretch out your loan term—sometimes to 40 years. That means you’ll be in debt for much longer and could end up paying more in total interest.

- The loan principal will increase through capitalization because the lender adds missed payments together with fees and penalties to your original loan amount.

A loan modification provides a path to keep your home, but it’s crucial to recognize it as a significant financial event that reshapes your debt and credit profile for years to come.

The main danger consists of needing to make payments on time after you finish your current payment schedule. Performance data reveals that 25 percent of modified loans develop into serious delinquencies within a few months after being modified. The third quarter of 2024 saw 7,450 loan modifications but 1,880 of these loans which represented 25.2% became 60+ days late or entered foreclosure within six months of modification. You can read the full research on mortgage metrics for a deeper analysis.

The modification process creates a situation where homeowners who struggle financially must extend their current financial problems instead of receiving proper assistance.

You need to evaluate alternative solutions because these risks seem too dangerous and the entire process appears to be a complete disaster. Homeowners who require a guaranteed fast solution can sell their houses for cash to get a fresh start. Our guide on the pros and cons of selling your house for cash can help you weigh this alternative. A cash sale provides a certain way out of mortgage debt without waiting on a lender’s decision.

Exploring Your Alternatives To Loan Modification

A loan modification serves as an emergency financial solution which does not work for all borrowers. You need to understand every available option before starting the lengthy process.

Every path offers different benefits and drawbacks which might suit specific individuals but not fit your needs. The correct decision depends on your present financial status together with your long-term financial goals. You should understand all main alternatives because this knowledge will help you select the best option for your situation.

Temporary Relief With Forbearance

You face an unexpected obstacle which includes losing your job for a brief period and getting an unplanned medical bill but you believe you will recover financially in the near future. Forbearance presents itself as an ideal solution for this situation. The program allows you to stop your mortgage payments for a few months while it reduces your payment amount.

Imagine it as a control which lets you freeze everything. Your lender agrees to let you skip or pay less for a set period, giving you breathing room. The key thing to remember is that those missed payments aren’t forgiven. The outstanding balance will become due at the end of your loan term or you can choose to pay it off through increased monthly payments or a single payment.

Starting Fresh With Refinancing

You should consider refinancing as an option when your credit remains strong and your income stays the same but you face a high-interest mortgage loan. The process involves obtaining a new loan with better conditions to pay off your current loan completely.

The purpose of this program is to help you get a lower interest rate which will decrease your monthly expenses. The program does not function as a hardship assistance program. Lenders will evaluate your financial information but they will probably reject your application because you have already missed payment deadlines. The program functions as a financial planning tool which helps people manage their money instead of serving as an emergency solution for urgent financial needs.

When You Owe More Than Your Home Is Worth

Sometimes, the housing market takes a turn and you find yourself “underwater”—meaning you owe more on your mortgage than what your home is actually worth. Short sale presents itself as an option when you need to sell your house but you lack sufficient funds to cover your loan balance. Your lender has approved you to sell your home for less than the amount you owe on your mortgage.

Short sale allows you to escape from an unmanageable mortgage without facing the severe consequences of a complete foreclosure but requires your lender’s full approval and results in substantial credit damage.

The approval process for short sales requires you to handle extensive documentation while you negotiate with your bank. Real estate professionals can better understand short sales through our guide which explains what is a short sale in real estate. The process provides a better solution than foreclosure but you should expect an extended period of uncertainty.

Comparing Your Foreclosure Prevention Options

Mortgage problems present such a wide range of choices which make it difficult to find the right solution. The table shows you the main differences between a loan modification and its most common alternatives so you can select the best path for your needs.

| Option | Best For | Impact on Credit | Keep Your Home? |

|---|---|---|---|

| Loan Modification | Homeowners with a long-term hardship who want to stay in their home. | Negative, but less severe than foreclosure. A “settled” status appears on your report. | Yes, if approved and you meet the new terms. |

| Forbearance | Short-term financial setbacks where your income is expected to recover quickly. | Minimal to moderate negative impact, as long as you fulfill the repayment plan. | Yes, this is a temporary pause. |

| Refinance | Homeowners with good credit and equity who want a lower interest rate. | Can be positive in the long run, but has a small, temporary dip from the credit inquiry. | Yes, you’re just replacing your old loan. |

| Short Sale | When you’re “underwater” and need to sell but can’t cover the full loan balance. | Significant negative impact, but usually less damaging than a full foreclosure. | No, you are selling the home. |

| Selling for Cash | Homeowners needing a fast, certain exit to avoid foreclosure and get a fresh start. | No direct negative impact. Your mortgage is paid off and closed as “paid in full.” | No, but it’s a voluntary sale on your terms. |

Your decision will depend on your top priority. Do you need to stay in your home at all costs, or is a clean financial slate more important?

Selling Your House Quickly For Cash

The extended time required for these methods along with their unpredictable results make them unsuitable for most home sellers. If you need a guaranteed exit from your mortgage without the stress of lender negotiations, repairs, or potential rejection, selling your house directly for cash is a straightforward, powerful alternative.

The route becomes a transformative solution when:

- You need to relocate quickly because of a new employment opportunity or family obligation.

- The property requires extensive repairs which exceed your current financial capabilities.

- You want to protect your credit score from the negative effects which occur when a home goes into foreclosure or short sale.

- You need financial certainty right now to pay off debts and move on.

Companies that buy houses for cash specialize in helping homeowners in these exact situations. The company provides fair cash offers to homeowners who can complete their home sales within weeks instead of waiting for months. One such company is Eagle Cash Buyers. This option lets you achieve a clean break because it frees you from debt while removing the emotional stress which comes from dealing with your lender.

When A Cash Sale Is The Right Move

A loan modification can be a lifesaver, but let’s be honest—it isn’t always the right answer. The treatment works as a bandage which covers deep wounds because it fails to address the core reasons which cause your financial difficulties to persist and your house to become more costly than beneficial.

When you find yourself in that spot, selling your home for cash can be the most practical and liberating decision you can make. The program enables you to terminate your mortgage stress while it grants you immediate control over your financial future.

Why A Cash Sale Might Be The Smarter Choice

A loan modification functions as a bank negotiation process which does not guarantee that your bank will accept your request. A cash sale empowers you to take complete control of the process. The solution offers an ideal option for homeowners who want to sell their property quickly with guaranteed results and without facing common home selling difficulties.

Check if you recognize any of these situations:

- You need to move, and fast. A job opportunity which offers a great career path or an urgent family situation across the nation requires you to relocate immediately without waiting for loan modification approval or home sale completion.

- The house requires costly major repairs. A cash buyer will purchase your property without any need for you to fix the roof or foundation or HVAC system because they will buy it as it stands.

- You just want a clean financial start. Selling for cash enables you to get money which you can use to pay off your mortgage and other debts while starting a fresh financial chapter without any home loan obligations.

- You need speed and certainty. With a cash sale, you skip the nerve-wracking process of open houses, picky buyers, and the risk of their financing falling through at the last minute.

A cash sale is a strategic decision. You will receive instant financial relief through a closed sale which lets you leave the loan modification process behind to build your future according to your preferences.

How A Quick Sale With Eagle Cash Buyers Works

The process of selling your home for cash money takes less time than most people think. The process of loan modification requires homeowners to understand every aspect of this path because they want to choose this option instead of getting a loan modification. Before making a final decision you should learn about proper due diligence procedures.

At Eagle Cash Buyers, Eagle Cash Buyers provides homeowners with a simple solution to sell their homes through their service. The process requires no agent fees and you can avoid public open houses while you skip all home repair responsibilities.

We’ll give you a fair, no-obligation cash offer. The entire sale process usually takes only a few weeks to complete when our offer meets your needs. Our guide on companies that buy houses for cash will help you evaluate our services against other companies. The approach provides instant financial relief which enables you to continue your life without the weight of that mortgage.

Frequently Asked Questions About Loan Modification

The loan modification process appears like a complex maze when you face financial difficulties. The following information will answer common questions from homeowners which will help you understand the process better.

How Long Does The Loan Modification Process Usually Take?

You need to remain patient because this process will not bring any immediate solutions. The application review process typically lasts between 30 and 90 days after you submit your complete application package.

But that’s a best-case scenario. The entire process will start over again when you need to provide additional documents or when your application lacks necessary information. Your best bet is to be meticulously organized and respond to any requests from your lender immediately.

Can A Modification Immediately Stop A Foreclosure Sale?

Yes, but the timing is absolutely everything. A loan modification stops a foreclosure process which lets you pause the process yet it does not grant you any magical powers. The federal rules require lenders to stop the foreclosure process when you submit a complete application at least 37 days before the scheduled sale date.

If you wait and apply any closer to the sale date, that protection might not apply, and the auction could proceed as planned. The lesson is clear: act the moment you know you’re headed for trouble.

A loan modification application is one of the strongest tools you have to pause foreclosure, but it’s not a guaranteed stop. A complete, well-timed application is your best line of defense.

What Happens If My Loan Modification Application Is Denied?

The denial letter will give you a severe emotional impact which makes you feel terrible. The situation continues to exist although the fight has ended. Your lender must provide you with official reasons which explain why they rejected your application and you should have the ability to challenge their decision. The process requires you to act quickly because you only have 14 days to file your appeal.

You need to start reviewing your alternative options when your appeal fails. Your options include short sale or home sale. A denial serves as a critical moment which requires you to understand all possible outcomes that can result from mortgage default.

Can I Qualify For A Modification If I Am Unemployed?

It’s definitely possible. Lenders assess your complete financial situation to determine your ability to make regular monthly payments regardless of the type of employment you have.

You must demonstrate a steady flow of income to qualify. All sources of cash flow which bring in stable money include unemployment benefits and disability payments and spouse income and pension distributions and retirement benefits. You can still get approval by demonstrating your ability to pay the modified payment amount.

You should find alternative solutions because loan modification processes take too long and produce uncertain results. One option is working with a company like Eagle Cash Buyers. We can make a fair cash offer for your house just as it is, letting you skip the lender headaches and close in as little as a few weeks. It’s a clean break that lets you settle your mortgage situation and move on. Learn more at https://www.eaglecashbuyers.com.