When facing foreclosure, the biggest question on your mind is often the simplest: how long do I have? The short answer is that the foreclosure process can take anywhere from a few months to over a year. The exact timeline depends on your state’s legal system and the particular foreclosure type as well as the actions you choose to handle the matter.

The Foreclosure Timeline: A Direct Answer

A person who faces foreclosure will experience feelings similar to being lost during a storm without any form of direction. The first step to finding your way forward requires you to establish a timeline. The program offers a vital period for you to discover your choices and seek professional guidance which will help you choose the best solution for your family.

The foreclosure process operates as a continuous sequence of events which leads to one of two possible outcomes based on your state of residence. Some paths are short sprints, while others are long, drawn-out marathons. The process starts at a later point in time than when you first missed a payment. In fact, under federal law, your lender generally has to wait until you are more than 120 days behind on your mortgage before they can even initiate the official foreclosure process. The system contains an inbuilt pause which allows users to discover their options while working to restore their previous status.

Key Stages at a Glance

The following information explains the standard foreclosure process through its individual stages. The sequence of events remains consistent yet the timing of each event can vary. Knowing where you are in the process helps you anticipate what’s coming next. The structure is similar to other legal timelines, like those that explain how long does probate take, where each phase has a purpose and a general timeframe.

Below is a quick overview of what to expect.

At a Glance: Key Stages of Foreclosure

| Foreclosure Stage | Typical Timeframe | Key Action |

|---|---|---|

| Pre-Foreclosure | 1-120+ Days | The grace period begins right after you skip a payment. You can catch up on what you owe before any formal legal action starts. |

| Notice of Default | 30-90 Days | The process starts when your lender submits a public document which shows your loan has defaulted. |

| Notice of Sale | 21-120 Days | The lender schedules an auction date for your property and notifies you and the public. |

| Auction/Sale | 1 Day | The property is sold at a public auction. Often, the bank itself is the highest bidder. |

| Post-Sale Period | Varies by State | This final phase includes any legally required “redemption period” or the start of the eviction process if you haven’t moved out. |

It’s clear that the consequences of mortgage default can be incredibly serious, which is why understanding this timeline is so important. The method allows you to take control instead of merely responding to situations.

A Step-By-Step Guide to the Foreclosure Process

The experience of foreclosure creates confusion but learning about the process will lead you to discover your way to recovery. The foreclosure process follows an organized sequence of events which leads to predictable outcomes. The path to control and suitable solutions becomes possible when you understand the necessary steps.

The journey actually begins long before you get an official notice in the mail. Your first missed payment will trigger a pre-foreclosure period of 120 days according to federal law which starts the countdown. This isn’t a penalty box; it’s a protected window of time for you to talk to your lender and explore options to get back on track.

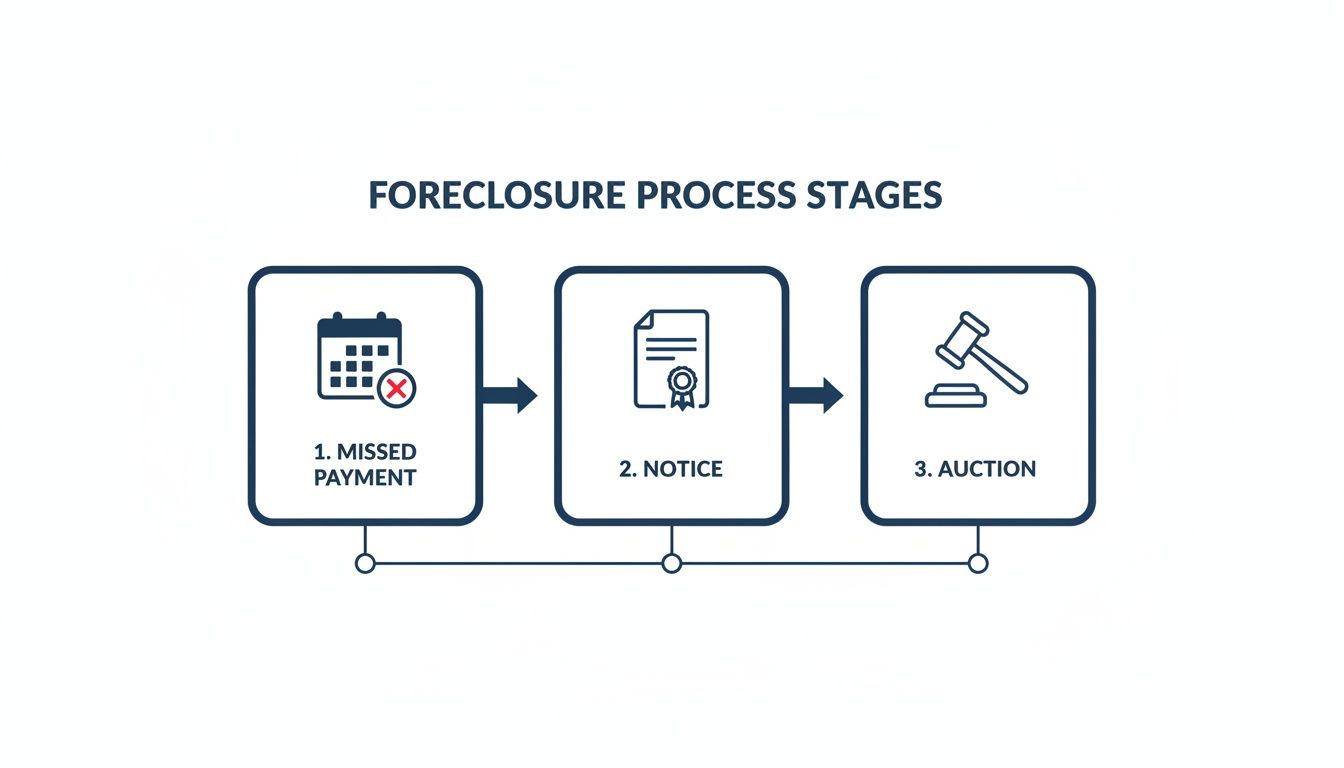

The simple diagram demonstrates the entire process which starts with your first missed payment and ends with the final auction.

The situation that begins as a simple disagreement between you and your lender will evolve into a public court case. That’s why acting early is so important.

The Official Start: Notice of Default

The lender will start the foreclosure procedure when the 120-day timeframe passes without any successful resolution. The process starts when the lender files a Notice of Default (NOD). The NOD serves as the legal starting point which begins the official legal process.

The NOD becomes public record after the lender files it and you will receive a copy. Your total debt amount appears in this document along with any outstanding payments and overdue penalties which you must pay within a specified time frame to resolve the default. The reinstatement period typically lasts between 30 and 90 days depending on the laws of your state.

This is your first real chance to stop the process before it picks up steam.

Key Takeaway: The time between receiving the Notice of Default and the home being scheduled for auction is your most critical window for action. Your options get much more limited once a sale date is set, so you have to move quickly.

The Path to Auction: Notice of Sale

The lender will proceed to issue a Notice of Sale if you fail to resolve the default by the given deadline. The public auction of your home will take place at the specified date and time and location which this formal announcement provides.

The timeline here can be surprisingly fast. In some states, the auction can happen in as little as 21 days after the notice is issued, while in others it might be several months away. You still have options, but the clock is ticking a lot louder now. While it might be possible to reinstate the loan just before the sale, it becomes much harder. Homeowners who reach this stage must learn the available options to stop a foreclosure auction from proceeding.

The Final Stages: Auction and Post-Sale Period

The auction or sheriff’s sale is where the ownership of your property officially changes hands. The highest bidder will purchase your home at the auction. The lender becomes the highest bidder when no other bidders participate at the required price level.

The process continues to exist after you complete the sale. Some states have what’s called a statutory right of redemption. The original homeowner receives this right to purchase back the property through full payment of the auction price together with all associated costs. The redemption period exists in select areas but it lasts for a very short time so you need to understand your state’s laws.

The new owner must begin a separate eviction process because you remain in the home after the sale has been completed and the redemption period has ended. The final stage of eviction requires court orders together with police involvement to carry out the authorized removal from your home.

Why Your State’s Laws Dictate the Timeline

Your zip code functions as the most essential element which determines the duration of your foreclosure process. The main reason for this difference stems from whether your state conducts foreclosures through judicial proceedings or handles them outside of court systems.

The United States divides its foreclosure system into two primary categories which include judicial and non-judicial foreclosure states.

A judicial foreclosure operates as a complete court case. The lender has to sue you in court, and a judge oversees every step. The process involves formal document submissions and court hearings and judicial decisions which extend the timeline to months and sometimes even years.

A non-judicial foreclosure operates as an administrative procedure rather than a judicial one. The lender can proceed with the foreclosure process without filing a court case because your mortgage contract contains a “power of sale” clause which exists in most states in these states. The process operates more quickly because it avoids the court system which tends to be overcrowded.

Judicial vs Non-Judicial Foreclosure States

The first step to estimate your personal timeline requires you to identify which system your state uses. A court-supervised process gives you more official chances to fight back, but that comes at the cost of living in limbo for a lot longer.

- Judicial Foreclosure: The lender must file a lawsuit. The states of New York Florida and Illinois follow this path but it usually takes longer than other options.

- Non-Judicial Foreclosure: No court approval is needed. The process runs quicker in Texas and California and Georgia which allows foreclosures to occur at an unexpected fast rate.

Because the legal hoops are so different, the answer to “how long does foreclosure take?” can change dramatically just by crossing a state line. The ability to locate case law provides you with essential insights into the established legal precedents which direct the procedure in your jurisdiction.

State Timelines Can Vary From Months to Years

The difference in timelines isn’t just a minor detail—it’s massive. The national average foreclosure timeline stands at 608 days which equals about one and a half years but this figure shows little value when viewed independently.

The state-specific data enables you to see the actual situation. The average foreclosure duration in Louisiana reached 3,632 days which equals almost ten years. West Virginia Texas Virginia residents experienced foreclosure proceedings that lasted between 135 and 160 days which equals about five months.

Key Insight: A state’s foreclosure laws are a reflection of its priorities. Some states build in more protections for homeowners, while others prioritize a lender’s ability to efficiently reclaim a property. The legal principle at the heart of this system leads to different timeframes for families to resolve their issues.

The vast difference between these numbers demonstrates why national averages fail to provide an accurate picture. Your state’s laws determine every step of the process starting from the initial notice you receive up to the final auction date.

How Your Actions Can Influence the Foreclosure Timeline

The state laws establish the fundamental rules for foreclosure but you remain in control as the driver of this process. The choices you make will determine the speed at which the process advances. In fact, you have far more influence over the timeline than most people realize.

Being proactive can buy you invaluable time to figure things out. Inaction leads to a feeling of rapid progression which limits your available choices. The first step to gain control over a difficult situation requires you to learn how your decisions affect the process.

Actions That Can Delay Foreclosure

You can take strategic actions to delay the process when you want to extend your time for exploring different options. Your most effective communication method to reach your lender serves as your most powerful instrument in this situation.

- Request Loss Mitigation: The moment you think you might have trouble making a payment, apply for loss mitigation. Lenders are legally required to review your application if you submit it at least 37 days before a scheduled sale, and this action officially pauses the process.

- You can negotiate with your lender to permanently adjust your loan agreement through loan modification which may include interest rate reduction or payment term extension. The application process stops the foreclosure process from continuing until the review process is finished.

- File for Bankruptcy: This is a major legal step, but filing for Chapter 13 bankruptcy triggers something called an “automatic stay.” The court issues an order which stops creditors from taking any further action including foreclosure. The court will grant you a few months to reorganize your financial matters through an approved repayment plan.

Your lender will recognize your active pursuit of a solution through any of these actions. That alone often makes them more willing to work with you.

Actions That Can Speed Up Foreclosure

Just as you can pump the brakes, certain behaviors can take them off entirely. The accelerated pace of this process shortens your timeframe for achieving successful results.

Avoiding your lender stands as the single biggest mistake that any homeowner can make. Your bank will assume you are not cooperating when you disregard their phone calls and certified mail. The law allows lenders to start the foreclosure process at their earliest convenience which forces homeowners into a defensive position.

Key Takeaway: Communication is your greatest asset. The lender will start the foreclosure process when a homeowner stops responding to their calls. You can negotiate payment plans with a responsive person who will help you buy time even if you cannot pay right away.

You can take control of the sale process if maintaining ownership of your home becomes impossible. Learning how you can sell a house during foreclosure can be incredibly empowering. You can find a buyer without having to follow the bank’s entire process. A quick sale can settle the debt and prevent the foreclosure from ever being finalized on your record, giving you a clean exit that you control.

What Are My Options to Avoid Foreclosure?

The sight of a foreclosure notice creates a sense of total defeat but it actually represents two different directions to choose from. Your financial situation becomes manageable because you can select a different path. Multiple powerful solutions exist which offer various benefits and trade-offs during different timeframes. The key is understanding them so you can make the best decision for your situation.

And you need to act fast. With foreclosure filings on the rise, knowing your options is more important than ever. The United States saw 68,794 properties enter the foreclosure process during the first quarter of 2025 which represents a 14% increase from the previous quarter. The numbers demonstrate that you must find a solution before the process advances too far.

Working Directly With Your Lender

Your first call should almost always be to your lender. Believe it or not, they’d rather not foreclose. It’s a messy, expensive process for them, too. The service providers will attempt to work with you to discover a solution.

The following list presents the standard ways you can investigate together:

- Loan Modification: This isn’t a new loan; it’s a permanent change to your current one. Your lender could lower your interest rate or lengthen your payment schedule to create more manageable monthly payments. The program works well for people who have experienced permanent changes to their earnings but want to stay in their current home.

- Forbearance: If you’ve hit a temporary rough patch—like a sudden job loss or a medical emergency—forbearance can be a lifeline. Your lender agrees to pause or reduce your payments for a set period, giving you the breathing room you need to recover financially.

- Short Sale: With a short sale, your lender allows you to sell the house for less than the total mortgage balance. The process requires multiple steps which need bank authorization but it protects your credit report from receiving a foreclosure mark.

- Deed in Lieu of Foreclosure: Think of this as voluntarily handing the keys back to the bank. You sign the property over to the lender, and in return, they cancel your debt. The entry will show up on your credit report but it carries less weight than a full foreclosure.

Each of these traditional options takes time and requires the lender’s full cooperation. The negotiation process can drag on for months, all while the foreclosure clock keeps ticking.

Key Insight: Your lender isn’t the enemy. The homeowners must keep their home to stop foreclosure because they have the incentive to do so. Your willingness to share financial details with honesty about your resolution approach will establish opportunities which you were previously unaware of.

A Faster, More Certain Path: A Cash Sale

Some homeowners find the extended waiting periods and uncertain bank negotiation process to be unworkable. The fastest and most predictable method to safeguard your credit involves selling your property to a cash buyer.

This approach cuts through the red tape. The process enables you to avoid bank approval requirements and home repairs and multiple property showings. The cash offer from Eagle Cash Buyers comes with a fair price and quick closing that typically takes a few weeks. The fast repayment process enables you to eliminate your mortgage debt while stopping foreclosure proceedings which results in cash earnings. The process delivers an absolute conclusion which eliminates all stress and uncertainty. The seven methods to stop foreclosure will help you decide which solution fits your situation best.

The following comparison shows different foreclosure alternatives which enable you to evaluate their benefits and drawbacks based on your objectives.

Comparing Your Options to Avoid Foreclosure

| Option | Best For | Typical Timeline | Impact on Credit |

|---|---|---|---|

| Loan Modification | Homeowners with a long-term income reduction who want to stay in their home. | 2-3 months | Minimal to none. |

| Short Sale | When you owe more than the home is worth and can’t afford payments. | 4-12 months | Significant negative impact. |

| Deed-in-Lieu | When you can’t sell the home and want a quicker resolution than foreclosure. | 2-4 months | Significant negative impact. |

| Selling for Cash | Homeowners who need a fast, certain sale to pay off the lender and protect their credit. | 2-3 weeks | None. The mortgage is paid in full. |

Ultimately, the best option depends entirely on your unique circumstances—how quickly you need to act, whether you want to keep the home, and what your financial picture looks like.

Common Questions About the Foreclosure Process

Even with a clearer picture of the foreclosure timeline, it’s natural to have more questions. This is a stressful situation, and the details matter. Our team has gathered the most important questions from homeowners to deliver direct answers that address their concerns.

Can a Foreclosure Auction Be Stopped at the Last Minute?

Yes, it is sometimes possible to stop a foreclosure sale, even just days before it’s scheduled to happen. One of the most common ways is to file for Chapter 13 bankruptcy. The filing of your bankruptcy case will trigger an automatic stay which immediately stops all debt collection activities including property auctions.

Another option is to get an injunction from a judge, but you’d have to prove the lender made a serious mistake in the process. Both of these are serious legal maneuvers that absolutely require an attorney’s help.

Frankly, waiting until the last minute is a high-stakes gamble. The best time to act is always in advance of the deadline.

How Long Do I Have to Move Out After a Foreclosure?

This really depends on your state’s laws. The new owner at the auction will be unable to change the locks. The new owner must follow the legal eviction procedure to force you out of your home.

Your door will get a “Notice to Quit” as the starting point of the process. The notice period ranges from 3 to 30 days before you must leave the property. The new owner must take legal action through an eviction lawsuit to have law enforcement remove you from the property if you fail to leave the premises. It’s wise to have a plan for where you’re going long before it gets to that point.

Will a Foreclosure Ruin My Chances of Buying a House Again?

A foreclosure definitely makes it harder to buy another home, but it doesn’t ruin your chances forever. Your credit report will show the foreclosure for seven years which creates a major obstacle for obtaining loans from lenders.

Most banks with conventional mortgage programs require you to wait between three and seven years after foreclosure completion before they will evaluate your application for a new mortgage. The FHA loan program through government-backed programs requires applicants to wait between three years and more depending on their financial stability.

The process of finding the right solution starts with learning about all your available options. Looking into the pros and cons of a short sale vs. foreclosure can help you choose a path that does less long-term damage to your financial health.

Facing foreclosure is tough, but you have options. A fast cash sale provides a straightforward solution for people who want to avoid the uncertainty of negotiations. The cash offer from Eagle Cash Buyers is both fair and their closing process is fast which can complete in as little as 21 days. The mortgage will become paid off which means the foreclosure process will stop completely and you will get to move on with your life without any damage to your credit. Get your no-obligation cash offer today.