One of the first questions homeowners ask after falling behind on mortgage payments is simple: how much time do I actually have? The answer fully depends on where you live and how quickly you act. Some foreclosures move in a few months. Others drag on for more than a year. State laws, lender procedures, involvement of the court, and your own decisions can affect the timeline.

The important thing to understand is this: foreclosure is not instant. There are multiple stages before the bank can take ownership of your home, and many homeowners still have chances to negotiate, to sell, or stop the process along the way.

The Basic Foreclosure Timeline

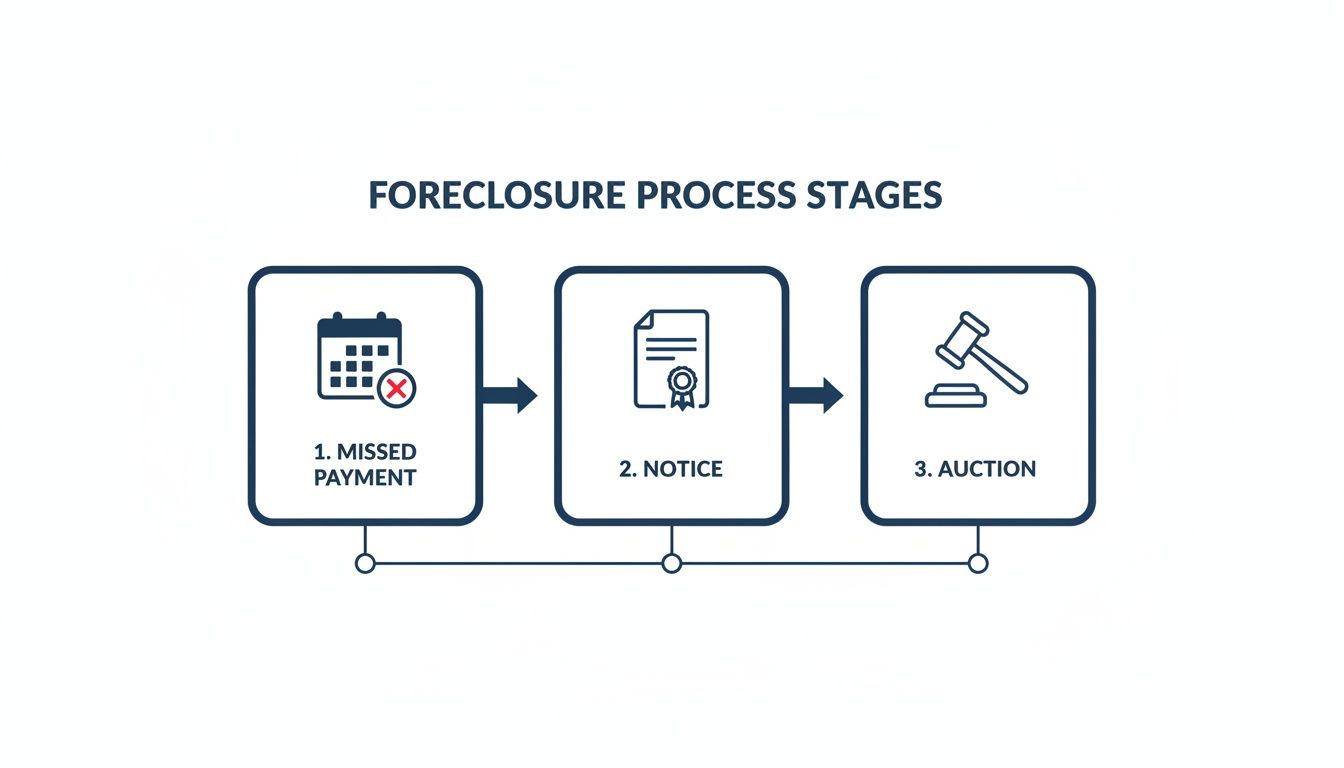

Most lenders can’t officially start foreclosure immediately after one missed payment. Federal mortgage servicing rules require lenders to wait for a 120 day delay in the payment before a formal process begins. This gives borrowers time to catch up, apply for assistance, or explore alternatives. The typical foreclosure process looks like:

Stage | Typical Timeline |

Missed payments/pre-foreclosure | 1-120+ days |

Notice of Default or lawsuit filing | 30-90 days |

Notice of Sale | 21-120 days |

Foreclosure auction | 1 day |

Post-sale eviction or redemption period | Varies by state |

It’s clear that the consequences of mortgage default can be incredibly serious, which is why understanding this timeline is so important. The method allows you to take actual control of everything.

The process can feel overwhelming because every stage brings new legal notices and deadlines. Dividing it into steps makes it easier to understand what will happen.

Step 1: Pre-Foreclosure Begins

Foreclosure technically starts after missed mortgage payments begin to accumulate. Most lenders attempt to communicate via phone calls, emails, and late notices. This early period is commonly called pre-foreclosure.

Many homeowners make the mistake of avoiding communication. In reality, speaking with a lender early usually creates more options.

Step 2: The Notice of Default

If the homeowner can’t resolve the delinquency, the lender files a formal legal notice. In many nonjudicial foreclosure states, this is called a Notice of Default. It becomes a public record, states how much money is owed, and provides a deadline to cure the default. And this period is the most important opportunity for the homeowner to stop the foreclosure. The seven methods to stop foreclosure will support you in deciding on the best solution for your case.

Step 3: Notice of Sale

If the default remains unresolved, the lender schedules the foreclosure auction. The homeowner is about to get a Notice of Sale with the auction date, time, location, and legal property details. Depending on state law, the auction may happen only a few weeks later.

Step 4: The Foreclosure Auction

The property is sold at public auction to the highest bidder. Possible buyers include:

- Investors;

- Cash buyers;

- Individuals;

- The bank itself.

If nobody bids high enough, the lender becomes the owner, and the property is REO (Real Estate Owned). Many foreclosure properties sell below full market value because buyers assume risks tied to repairs, title issues, and occupant removal.

Step 5: After the Sale

Foreclosure does not always end at the moment the auction finishes. Some states allow a redemption period where the homeowner can reclaim the property by paying the debt plus additional costs. If the homeowner remains in the house, the new owner must usually begin formal eviction proceedings.

Why State Laws Matter So Much

Foreclosure timelines differ a lot based on the state, because the systems themselves differ. For example, judicial foreclosure states, such as Florida and New York, require the lender to sue the homeowner in court.

Nonjudicial foreclosure states, such as California, Texas, and Georgia, avoid the courtroom completely and use a power of sale clause inside the mortgage agreement. The difference is massive. Some states average foreclosure timelines under 6 months, while others need several years. The ability to locate case law provides you with essential insights into the established legal precedents that direct the procedure in your jurisdiction.

How Your Actions Affect the Timeline

Foreclosure timelines are not completely fixed, and you can influence how quickly or slowly the process moves. For example, submitting a loss mitigation or loan modification can pause the activity while the lender reviews the request.

Filing bankruptcy triggers an automatic stay, which temporarily stops foreclosure proceedings immediately. Further, lenders generally work more cooperatively with borrowers who stay engaged and responsive, so negotiation is also an option.

Options to Avoid Foreclosure

Foreclosure auctions are not the only outcome available. In that situation, you can go for the following:

- Loan modification – A permanent loan adjustment that makes payments affordable again;

- Forbearance – Temporarily pauses or reduces payments during short-term hardship situations;

- Short sale – A short sale allows the home to sell for less than the remaining mortgage balance with lender approval. Looking into the pros and cons of a short sale vs. foreclosure can help you choose a path that does less long-term damage to your financial health;

- Deed in lieu of foreclosure – Voluntary transfer of ownership to the lender in exchange for debt forgiveness.

Some homeowners prefer to sell proactively instead of waiting for foreclosure to progress. These options can help owners to preserve equity and avoid auction losses.

Why Some Homeowners Choose Cash Buyers

Traditional home sales may need months, more specifically when repairs, inspections, and delays are involved. Foreclosure deadlines often leave homeowners without that much time. Cash sales simplify the process, because:

- Closing happens quickly;

- Financing approval is not needed;

- Repairs are usually not included;

- The lender gets paid faster.

Learning how you can sell a house during foreclosure can be incredibly empowering. You can find a buyer without having to follow the bank’s entire process.

Can Foreclosure Be Stopped Last Minute?

Sometimes yes, but this fully depends on the timing and circumstances. However, it is not okay to wait until the final days, because this creates a huge risk. Better act earlier.