Title insurance offers financial protection to property owners and their lenders by covering any monetary losses which result from previous ownership disputes with the property. The service protects your property rights through a single payment which you make during your closing process. The service protects your property rights from all previous debts and liens and fraudulent activities and other problems which might affect your home ownership. The document verifies that you have received complete ownership rights for the home purchase.

Understanding the Basics of Title Insurance

Title insurance operates as a distinct insurance type which differs from all other insurance products that most people understand. Your car insurance provides protection for upcoming accidents while health insurance covers all upcoming medical expenses. Title insurance functions differently because it investigates past events which affect the property to defend you from hidden problems that exist before anyone can discover them.

When you buy a house, you’re really buying the legal right to own it, which is called the “title.” A clean title proves that you have absolute ownership of the property because no other person holds any legal rights to it. Property ownership records span multiple years while they conceal various major incidents which occurred in the past.

The Role of a Title Search

The title company conducts an extensive investigation of public records before creating any insurance documentation. The researchers conduct an extensive title search which involves examining property records that span multiple decades including deeds and mortgages and tax records and court judgments and divorce decrees. Their goal is to find any red flags tied to the property, which is a crucial part of a smooth property ownership transfer.

The most thorough search methods still fail to guarantee complete accuracy in their results. The public records system fails to show certain problems which include forged signatures on historical documents and the emergence of unidentified heirs and mistakes which occurred during office work three decades ago. Title insurance offers you protection when you need it most. The financial backstop protects these hidden risks from creating any negative impact. For a deeper look into this process, check out this guide on The Role of Title Companies in Real Estate Sales.

KeyTakeaway: A title search is like a background check on your new home’s legal past. Title insurance provides protection to homeowners when background checks fail to identify ownership threats which endanger both property ownership and investment value.

The protection requirement stands firm for almost all real estate deals which include standard home sales and cash property sales. The base for a protected sale exists in clear and insurable titles because they let the buyer receive property ownership without future legal issues stemming from previous property histories.

Owner’s Policy vs. Lender’s Policy Explained

Title insurance exists as more than a single product according to how people discuss it. Two distinct types of real estate protection exist which defend homeowners as well as mortgage lenders during property transactions. Real estate buyers and sellers need to understand the main differences between these two concepts to succeed in their business.

The discussion starts with the lender’s policy. Your mortgage lender needs you to get this because it functions as a mandatory requirement. Think of it as the bank’s personal security blanket. The policy protects their financial investment in your property while it safeguards their loan from any concealed title defects.

The lender’s policy protects the remaining loan amount when an unexpected claim shows up after the property sale has closed. But here’s the critical part: it does absolutely nothing to protect your investment or the equity you’ve built. The other policy solution becomes necessary at this stage.

Why An Owner’s Policy Is Your Personal Shield

The owner’s policy exists as the next topic of discussion. People should not skip this step because it remains technically optional yet carries a high level of risk. The policy exists to defend your rights as a homeowner. Your legal ownership rights to this property remain protected through title insurance until you or your descendants decide to stop owning the property. You make one payment during closing which covers all costs for this insurance.

Here’s a real-world example of why it matters. You purchased your perfect home but after one year an heir from the previous owner emerged with a valid will which proved their ownership rights to the property. The absence of an owner’s policy would force you to spend tens of thousands of dollars on legal expenses to prove your property rights while risking both your house and all equity you have accumulated. An owner’s policy protects your financial interest by covering all legal expenses which arise in these situations.

Property inheritance involves complicated processes which include understanding mortgage effects when property owners pass away which makes lender’s policy mandatory for banking institutions. The owner’s policy stands as your strongest protection against sudden property-related issues.

The two policies have different features which I will now explain to you.

Owner’s Policy vs. Lender’s Policy

| Attribute | Owner’s Policy | Lender’s Policy |

|---|---|---|

| Who It Protects | The homeowner (buyer) and their heirs. | The mortgage lender. |

| Is It Required? | Optional, but highly recommended. | Required if you have a mortgage. |

| How Long It Lasts | As long as you or your heirs own the property. | Until the mortgage is paid off. |

| Payment | One-time premium paid at closing. | One-time premium paid at closing. |

The lender’s policy functions to protect bank funds while the owner’s policy defends both your home and your financial assets.

Who Pays For Each Policy?

So, who foots the bill? The answer to this question depends on two main factors which include regional business practices and the terms that parties reach during their property sale agreement.

- Lender’s Policy: The buyer generally covers the lender’s policy cost because it becomes part of their closing expenses. The loan agreement requires this condition to be met before you can get the money.

- Owner’s Policy: This is up for grabs. The seller usually pays for the owner’s policy in various markets because this practice shows they will deliver a clean title to the buyer. The buyer needs to handle this expense in different regions.

Homeowners who face financial difficulties because they might default on their mortgage find it challenging to handle additional costs when they decide to sell their property. The search for straightforward solutions with minimal negotiation requirements motivates sellers to choose this approach. You have the option to sell your home to a cash-buying company through this method. The process becomes easier when companies like Eagle Cash Buyers handle all standard closing costs including title insurance expenses. The cash offer you receive represents the complete amount which you will receive thus giving you financial stability during your time of need.

What Title Insurance Actually Covers—And What It Doesn’t

You need to pay for what exactly? Title insurance functions as a protective barrier which defends you from any previous property ownership issues. The policy exists to defend you from previous events which could threaten your property ownership rights today.

Your policy exists to protect you from any issues which might emerge with your property ownership rights. The term refers to any historical issue which remains unresolved thus reducing the value of your property claim. These gremlins exist hidden within public records which homebuyers cannot detect during their standard property search thus making this insurance essential.

What Is Typically Covered

Title insurance policies offer protection to property owners against multiple hidden risks which existed before they obtained property ownership. The entire point is to make sure you have a clean, undisputed claim to your property.

Here are a few of the most common issues a standard owner’s policy is built to handle:

- Undisclosed Liens: Think of lingering debts attached to the property. The property might contain unpaid contractor bills which are called mechanic liens or it could have overdue property taxes or HOA fees that the previous owner failed to pay.

- Forged Documents: It’s more common than you’d think. A forged signature on a deed which dates back several decades would make the entire sale invalid and this would endanger your right to own the property.

- Errors in Public Records: Public records contain errors which result from simple typing mistakes or document submission errors at the county recorder’s office that will create major legal problems after many years pass.

- Surprise Heirs: A previous owner’s distant relative might show up out of nowhere to claim their legal right to part of the property.

- Illegal Prior Deeds: The previous sale might have been authorized by someone who lacked legal authority because they were a minor or they lacked mental competence or they exceeded their selling authority.

The lack of title insurance will force you to pay all legal expenses which defend your property ownership rights. The situation requires payment of tens of thousands of dollars yet there exists a genuine possibility of property loss. Our guide on common title problems which disrupt closings will show you how to handle these situations.

Key Insight: A huge part of title insurance’s value isn’t just the payout if you lose; it’s covering the crushing legal bills required to defend your ownership in court in the first place.

Common Exclusions in a Title Policy

You need to understand both the protection and the limitations which title insurance provides. The program operates as a specialized system which protects your home but it does not offer complete coverage for all home protection needs.

The policy focuses on past risks so it will not provide coverage for these following situations:

- Problems That Arise After You Buy: Title insurance exists to protect against past events. The buyer must handle all liens and claims and issues which occur because of your actions or inactions after the closing date.

- Zoning and Building Permit Violations: Title insurance will not protect you if you find out that the previous owner constructed a deck without proper authorization or that your shed breaks zoning rules. Those are municipal or code enforcement issues.

- Anything from Your Home Inspection: A leaky roof, a cracked foundation, or faulty wiring? Those are physical problems with the house itself, which are covered by a home inspection (before you buy) and homeowners insurance (after you buy).

- Known Defects: The title search process reveals specific problems before closing but these issues become policy exceptions which do not receive coverage.

You can understand the function of title insurance in the overall system after you learn about its operational boundaries. The system requires this essential component to function because it works together with home inspections and insurance policies to provide complete buyer assurance.

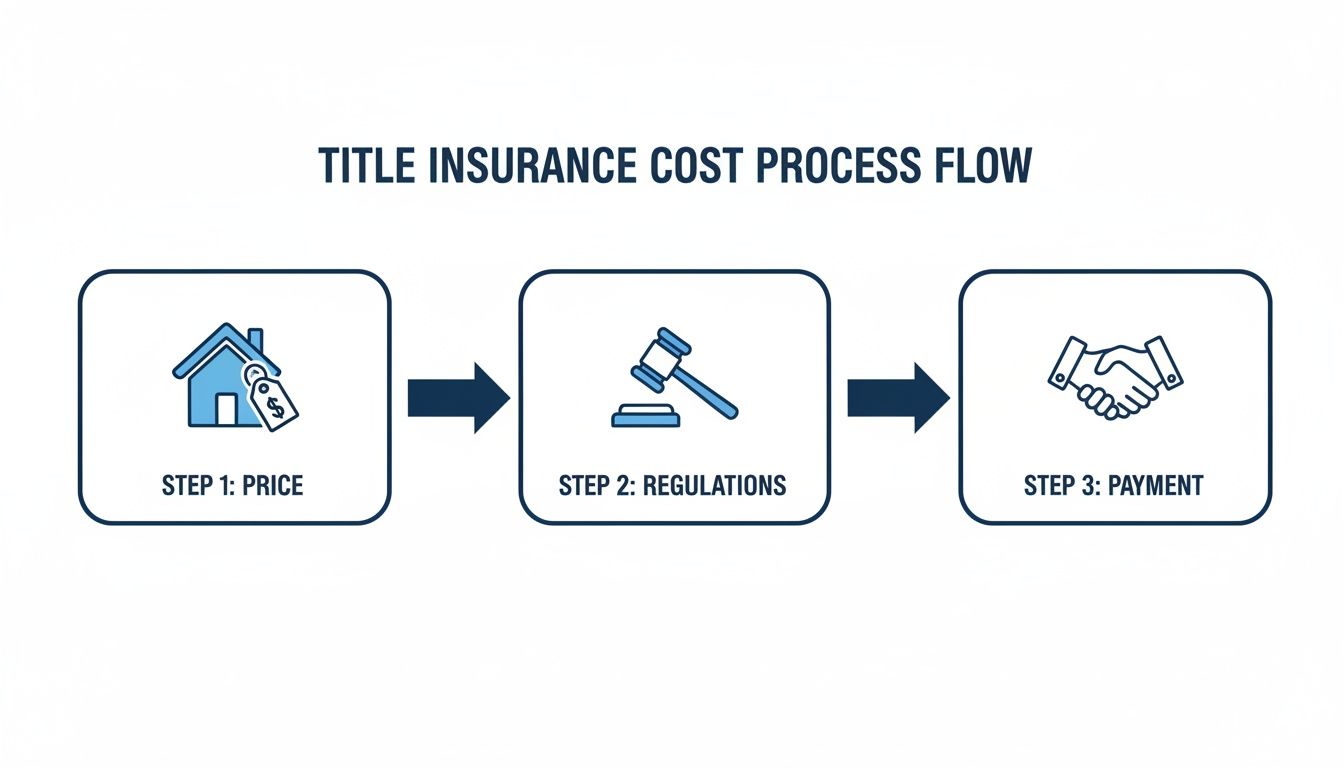

How Title Insurance Costs Are Calculated and Who Pays

The total protection cost becomes what? Let’s get into the dollars and cents.

One of the biggest misconceptions about title insurance is how you pay for it. Title insurance requires a single payment which you make during your property closing instead of monthly payments like your car insurance and homeowner’s policy. The payment provides you with protection which lasts throughout your home ownership and extends to your heirs after you pass away.

Breaking Down the Premium Factors

The cost doesn’t exist as an arbitrary number which someone made up. The calculation depends on two main factors which include the property’s sale value and the location of the property within state boundaries. States have established regulations which control title insurance pricing so customers should not experience large cost differences between different title providers.

The insurance cost increases because higher property values create greater financial risk for insurers to provide coverage.

As a general rule of thumb, you can expect the total cost for both the owner’s and lender’s policies to land somewhere between 0.5% and 1.0% of the home’s purchase price.

So, what are you actually paying for? The total cost typically bundles a few key services together:

- Risk Premium: This is the core insurance part of the policy. The insurance policy provides coverage for all expenses which arise when you need to defend your title against claims that emerge in the future.

- Title Search Fee: This fee pays for the detailed, meticulous work of digging through public records to find any potential issues before you close.

- Closing or Settlement Fees: These fees represent the administrative expenses which occur during the process of completing all necessary documentation to finish the purchase.

The all-in-one structure provides protection through one payment which covers both initial research expenses and ongoing financial security.

Who Typically Pays for Title Insurance?

Alright, so who writes the check? The answer depends on how people do business in their area and what parties agree to during their property sale negotiations.

A Common Scenario: While it can vary from one county to the next, it’s very common for the seller to pay for the owner’s title policy. The practice serves as a demonstration of their commitment to deliver a marketable title which is free from defects. The buyer needs to handle this expense in different regions.

This is a key negotiating point in any real estate deal. Homeowners who want to avoid complicated sales processes find negotiating these expenses to be very frustrating. The need for certainty becomes most critical when you sell your home because of divorce or sudden moves or when you inherit property.

The direct cash buyer method offers sellers the ability to avoid negotiations and additional expenses. Eagle Cash Buyers provides sellers with a direct cash offer while they handle all standard closing costs which include title insurance expenses. The cash amount you receive will match the number we provide to you. Our breakdown of typical cash buyer closing costs will help you understand what this amount covers. The process provides a simple method for selling your property which guarantees a successful sale without any unexpected problems.

The Role of Title Insurance in a Fast Cash Sale

The cash sale of your home should not make you believe that you can avoid essential procedures because you might think title insurance falls into this category. But in reality, it’s quite the opposite. Serious cash buyers refuse to proceed with deals unless they obtain a property which has an unblemished and insurable title.

The main benefit of cash sales comes from their ability to complete transactions at a fast pace. These transactions avoid the extended mortgage underwriting process yet their quick pace creates no space for any unforeseen events. A professional cash buyer needs to know, without a doubt, that they’re getting a property with a clear ownership history. Title insurance functions as the final seal which enables buyers to finish their deals with complete self-assurance and at an accelerated pace.

Why Cash Buyers Prioritize a Clean Title

The requirement for a clean title benefits homeowners who face difficult situations because it helps them avoid foreclosure and sell inherited homes and move quickly. The document guarantees your deal will remain secure because it prevents any unexpected problems which might occur due to previous legal matters from causing the deal to collapse at the last moment.

Title insurance is a one-time premium that shields both homeowners and lenders from hidden issues that could threaten ownership long after the keys are exchanged. Think of things like liens, undetected heirs, or even outright fraud. The fact that the U.S. title insurance industry generated $8.5 billion in direct premiums in just the first half of a recent year highlights how essential it is for secure real estate deals. For cash buyers who rely on local title companies to close fast, this protection is invaluable. You can read more about these industry trends on National Mortgage News.

Key Advantage: When a cash buyer requires title insurance, it means that once the sale is final, it’s truly final. For you as the seller, that means walking away with your money and the confidence that no old property claims will ever come back to haunt you.

This chart breaks down how the final cost of a title insurance policy comes together.

As you can see, the premium is based on the home’s sale price, set according to state regulations, and paid in a single lump sum at closing.

How Direct Buyers Can Make the Process Seamless

This is where working with a direct buyer can be beneficial. It allows you to skip the back-and-forth negotiations about who pays for what, as a reputable cash-buying company often takes care of it.

For example, at Eagle Cash Buyers, we have strong relationships with trusted local title companies. This lets us push the title search and insurance process through quickly, often well within our standard 21-day closing timeline. We also cover all closing costs, including the title policy.

The cash offer you see is the exact amount of cash you get. No hidden fees, no last-minute deductions. If you want to dive deeper, you can learn more about how companies that buy houses for cash operate and what to expect. It’s a truly streamlined approach designed for a guaranteed closing, free of the headaches that can derail a traditional sale.

Common Questions About Title Insurance for Sellers

Let’s be honest, the closing process can feel like you’re trying to learn a new language, and “title insurance” is one of those terms that trips a lot of people up. To cut through the confusion, here are some straight answers to the questions we hear most often from sellers.

Why Do I Need Title Insurance if a Title Search Was Already Done?

This is probably the most common—and most logical—question out there. You paid for a thorough search of the property’s history, so why shell out more for an insurance policy?

It helps to think of it this way: a title search is like a very detailed home inspection for your property’s legal history. It’s fantastic at uncovering known problems listed in public records. But just like a home inspector can’t see what’s lurking behind a wall, a title search can’t spot issues that are hidden from view.

Title insurance is your protection against what the search can’t possibly find. These are often called “hidden defects,” and they can be serious.

- Forgeries: Imagine a fake signature on a deed from 30 years ago. That one fraudulent act could potentially invalidate every sale that came after it.

- Undisclosed Heirs: A long-lost cousin of a previous owner could suddenly appear with a legitimate claim to the property.

- Filing Errors: Simple human error happens. A county clerk could misfile a document, creating a legal mess that might not surface for decades.

The title search is about minimizing risk. The insurance policy is about eliminating it. If one of these ghosts from the past ever shows up, the insurance company takes the financial hit, not you or the new owner.

Can a Title Problem Actually Stop My Home Sale?

Yes, it absolutely can. A major problem with the title—what people in the business call a “cloud on title”—can bring a sale to a screeching halt. Lenders simply will not approve a mortgage for a property with a title issue, and a cash buyer isn’t going to risk their capital on a property with a murky ownership history.

Things like unpaid contractor’s liens, a property line dispute with a neighbor, or an unresolved claim from a past owner all need to be cleared up before closing. The title company’s job is to spot these “clouds” and then work with you to resolve them so the property can be transferred free and clear.

Does a Cash Buyer Still Need Title Insurance?

It might seem odd since there isn’t a lender involved, but for a professional cash buyer, title insurance is completely non-negotiable. It’s how they protect their investment and guarantee they are getting undisputed ownership. For you, the seller, this is actually a huge plus.

A cash buyer’s insistence on a clean, insured title is your assurance that the deal is secure. It prevents last-minute collapses due to historical legal issues, providing the certainty needed for a fast and reliable closing.

The requirement creates an unbreakable bond between the two parties which lets you take your money while preventing any future claims from surfacing. The entire $17.1 billion title insurance industry is built on providing this kind of certainty. The real estate sector has demonstrated its vital importance because it generated $8.5 billion in insurance premiums during the first six months of the current year. The website ibisworld.com provides information about the size of the title insurance market.

How Long Does My Owner’s Policy Last?

Your owner’s title insurance policy is good for as long as you or your heirs own the property. The policy requires only one payment which you make during the closing process to receive complete protection for your entire life. The policy continues to provide protection against specific legal claims which occur after you have sold your property.

You need to select between two options when you want to sell your home because you have title issues. You have several options. You can solve any problems through cooperation with real estate agents and title experts or you can select different selling approaches which provide faster transactions and simpler processes.

A direct cash offer represents one of the available options. This method suits people who want to expedite their sale process while receiving a guaranteed payment for their property. Eagle Cash Buyers purchases homes regardless of their condition and they cover all closing expenses including title insurance fees while their typical closing period lasts about 21 days. Get your fair, no-obligation cash offer today at https://www.eaglecashbuyers.com.