A foreclosure auction is the final stage of the foreclosure process. When a person who owns a home can’t pay the mortgage payments, the lender can force the property into a public sale to recover the remaining loan balance.

For homeowners, the word auction usually feels overwhelming. The good part here is that foreclosure is not something that can be completed overnight, not at all. It follows a legal timeline with notices, waiting periods, and opportunities to stop the sale before it happens. Understanding how foreclosure auctions work gives you something important back, and this is clarity. Once you know the process, the deadlines, and your rights, you can make the proper decisions.

What Is a Foreclosure Auction?

A foreclosure auction is a public sale where the property goes to the person or company that bids the highest. The auction may involve:

- Real estate investors;

- Cash buyers;

- Individuals looking for discounted homes;

- The bank itself.

The lender’s goal is simple – to recover as much of the unpaid mortgage debt as possible. If nobody bids enough money, the lender takes ownership of the property. The home then becomes “REO” (Real Estate Owned), meaning the bank officially controls it and will likely try selling it later through a real estate agent.

Who Is Involved in the Auction Process?

Several parties play key roles during foreclosure auctions. They all have influence on how the process is about to go:

Participant | Role |

Lender | Attempts to recover unpaid debt |

Trustee or Sheriff | Conducts and supervises the sale |

Bidders | Investors or buyers trying to purchase the property |

Homeowners | Original property owner facing foreclosure |

Sometimes foreclosure auctions look chaotic from the outside. However, they actually follow a strict legal process.

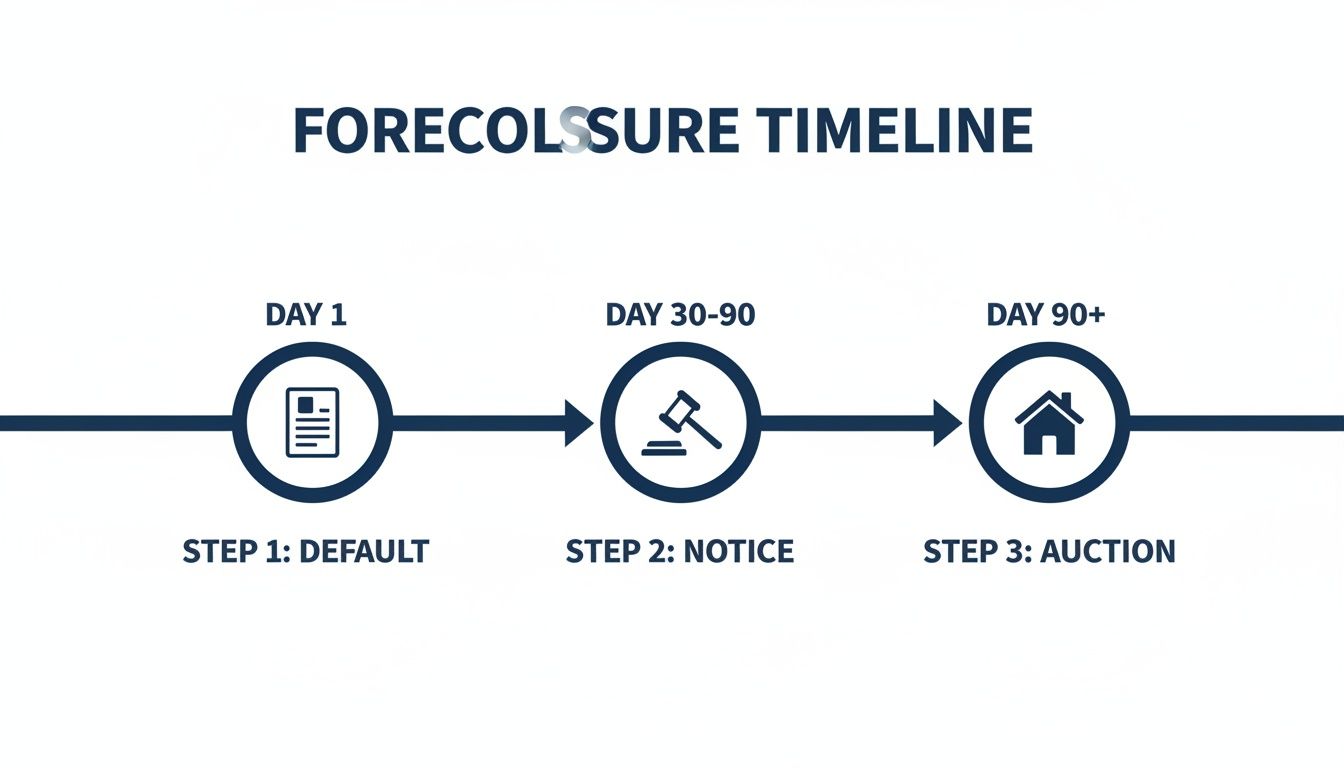

The Timeline Before the Auction

Foreclosure is not happening immediately when you can’t send 1 payment. Federal mortgage servicing rules usually prevent lenders from officially starting foreclosure until the borrower is over 120 days delinquent. This is also called the 120-days rule. That window exists to give homeowners time to:

- Catch up on payments;

- Apply for loan modifications;

- Negotiate with the lender;

- Sell the property;

- Seek legal assistance.

If you take action earlier, you will have more options. You will receive missed mortgage payments and pre-foreclosure notices. To ignore these is one of the main mistakes a homeowner makes. Silence often speeds up foreclosure instead of delaying it.

Once the lender officially starts foreclosure, homeowners receive legal notices. The exact document depends on the state. Nonjudicial states issue a Notice of Default, while judicial states involve a lawsuit and court complaint. At this point, foreclosure is public record.

It is essential to know how long the foreclosure process takes, so you can take some steps. If the default is not resolved, the lender schedules the auction, and on the notice of sale, you will see the date and time of the auction, the property location, and legal sale information.

Judicial vs. Nonjudicial Foreclosure

Not every foreclosure follows the same process, and it is very important to know the difference. It depends on the state and whether it is judicial or nonjudicial.

Judicial Foreclosure

For judicial foreclosure, a lawsuit must be filed by the lender. The court oversees the process from the beginning to the end, which makes it slower. Judicial foreclosure states often provide homeowners with:

- More legal protection;

- Additional time for response;

- Court hearings;

- Opportunities to challenge the foreclosure.

States like Florida, New York, and Illinois use judicial foreclosure systems most of the time. These are the better ones.

Nonjudicial Foreclosure

Nonjudicial foreclosure happens outside the courtroom. The lender relies on a power of sale clause already included in the mortgage documents. This process moves much faster, because there is no need for court approval. States such as California and Texas often use nonjudicial foreclosure systems.

What Happens on the Auction Day?

Foreclosure auctions usually take place at county courthouses, inside the government buildings, or at the office of the sheriff. Most buyers who attend are experienced investors. The process is fast. It begins with the starting bid amount, then goes into competitive bidding, and then either a third-party buyer wins or the bank takes the property.

Your Rights as a Homeowner

Even during foreclosure, homeowners still have legal rights. These include:

- Right to Notice – Lenders must provide proper written notice before scheduling foreclosure sales. Failure will delay or invalidate the process.

- Right to Reinstate the Loan – Many states allow homeowners to stop foreclosure by paying missed mortgage payments, late fees, and legal expenses.

- Right of Redemption – Some states allow homeowners to reclaim the property even after auction if they pay full debt plus additional costs.

These vary based on state law. You’d better check the law of your state first.

Alternatives to Foreclosure Auctions

Foreclosure auctions are not the only outcome available. People can get a loan modification, ask for forbearance, or even for a short sale. In some situations, you can actually sell your house during foreclosure, if the lender allows that.

Selling before the auction becomes the cleanest solution for most homeowners. The traditional sale may work if you have enough time, but foreclosure deadlines often need direct cash buyers. Cash sales close quickly, eliminate repair requirements, and avoid financing delays. The use of proven techniques to boost property value will enhance your selling position when the time comes to sell.

Can You Stop a Foreclosure Auction Last Minute?

Sometimes yes, but it depends on the situation. This guide on how to delay foreclosure will give you specific effective strategies to protect your home. Basically, you can stop the foreclosure through:

- Bankruptcy filing;

- Loan reinstatement;

- Selling the property;

- Negotiating directly with the lender.

However, waiting until the final days creates a huge risk. If you take action early, you will have more control over the outcome. Foreclosure auctions move fast once the legal process reaches its final stage. So it is essential to understand the system early so you can have the best chance to protect your home.