Maintaining the payments of mortgages can be challenging when financial issues appear. In such a circumstance, people who have homes tend to find a way of escaping foreclosure. A common solution is a loan modification. The latter is described further on this page.

What Is a Loan Modification in Simple Terms

A mortgage is a long-term agreement based on your financial situation at the time you signed it. But life always changes, and sometimes those original terms no longer work. A loan modification comes as a change to your current contract. This is not a new loan, so it is not refinancing.

Rather, your lender modifies the conditions of your current loan so that it becomes easier to make payments. This is aimed at lowering the monthly payment to avoid foreclosure and retain your home.

How a Loan Modification Works

The main purpose of the loan modification is to lower your monthly mortgage payment. Landers can do that in multiple ways. These involve:

- Making an interest rate smaller;

- Extending the loan term;

- Forbearing part of the loan.

After approval, these changes replace your original mortgage default systems. Still, you owe the debt, but the structure itself becomes more manageable.

Why Loan Modifications Exist

This solution became trendy after the 2008 financial crisis. Many homeowners were unable to keep up with mortgage payments due to falling property values, job losses, and more reasons.

Foreclosures became a major issue for both families and lenders. As a result, lenders and governments created programs to let people keep their homes rather than losing them.

The idea remains simple. Foreclosure is expensive and harmful for everyone. Loan modifications help borrowers avoid losing their homes. Meanwhile, it allows lenders to recover payments in a more stable way. This is also about proper due diligence procedures and similar nuances.

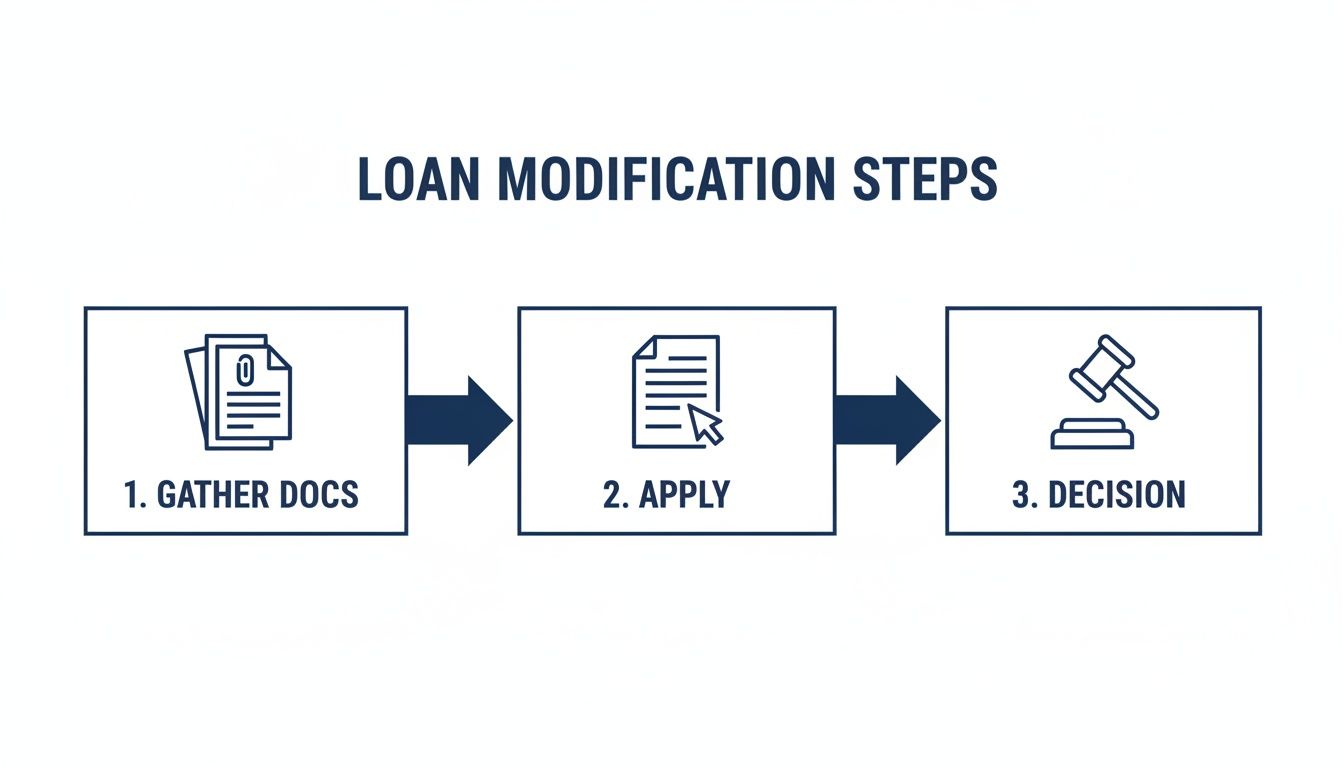

Navigating The Loan Modification Application Process

In order to get a modified loan, you need to work closely with your lender. The procedure itself is based on proving two things: you are experiencing financial problems, and you can afford the new reduced payment. The procedure often starts when you reach your mortgage servicer and request an application.

Proving Your Eligibility

Lenders will ask why you are trying to cover a mortgage. The most common reasons involve:

- Job loss or reduced income;

- Divorce or death in the family;

- Medical expenses;

- Unexpected financial emergencies;

- Natural disaster.

Along with that, do not forget to mention that you can afford the changed payments going forward.

Assembling Your Financial Story

To make sure the procedure will be smooth and fast, prepare and then provide several documents. The list consists of:

- Official proof of your current income;

- Recent tax returns;

- Bank statements;

- A hardship letter explaining your situation;

- A monthly budget showing income and expenses.

Remember that the undone paperwork is among the primary causes of delaying or rejecting applications. This means accuracy is very important.

Homeowners who want to stop a foreclosure auction should learn how to stop a foreclosure auction. That’s because filing for an application does not mean the automatic stop of the procedure.

Pros and Cons of Loan Modification

Depending on the situation, a loan modification may bring numerous benefits. Nevertheless, it also has specific drawbacks. Here is a full list of both:

Pros | Cons |

Helps you avoid foreclosure | Approval is not guaranteed |

Lowers monthly mortgage payments | The process can take months |

Allows you to keep your home | Requires a lot of paperwork |

Can reduce financial stress | A credit score may still be negatively affected |

Less damaging than foreclosure on your credit |

Overall, there are more advantages than weak points. Plus, the solution has numerous alternatives, and you can learn the pros and cons of selling your house for cash, for instance.

Alternatives to Loan Modification

Firstly, we recommend browsing through the full research on mortgage metrics. If you decide that an alternative is needed, select any of these solutions:

- Forbearance. It allows pausing or reducing payments temporarily. Nevertheless, misstated transfers must be repaid later.

- Refinancing. The option changes the current loan for a fresh one. It is usually only available if you still hold strong credit and a stable income.

- Short Sale. If you owe more than the price of your home, a short sale in real estate lets you sell the property for less than the mortgage balance with lender approval. It still affects your credit, yet avoids full foreclosure.

Weigh all these options and then choose the most appropriate one, based on your circumstances.

Selling Your House for Cash

For some homeowners, selling their homes quickly for cash feels like the right solution. Plus, this is a good alternative to loan modification.

A cash sale means selling your home “as-is” without repairs, cleaning, or agent fees. The buyer purchases the property directly. Usually, that happens within 2–14 days. Take advantage of this solution when:

- You need to do everything quickly;

- The home requires expensive repairs;

- You strive to avoid foreclosure;

- Immediate financial relief is required.

Cash buyers manage most of the processes involved, and there is no waiting for bank approvals. Learn more at https://www.eaglecashbuyers.com.

FAQ

How long does the loan modification process take?

In the majority of situations, lenders will need approximately 30 to 90 days to process a full application. But there are delays all around.

Can a loan modification stop foreclosure right away?

The solution can pause foreclosure. If you provide a completed application at least 37 days before a scheduled foreclosure sale, lenders are often required to pause the procedure.

What happens if my loan modification is denied?

Your lender must explain why the request was rejected. Usually, you have around 14 days to appeal the decision.

Can I qualify for a loan modification if I’m unemployed?

Yes, lenders focus on whether you have a stable source of income, not a job itself.